Can you sue your own insurance company? Yes, you can. If your insurer denies a legitimate claim, offers an unfair settlement, or engages in bad faith practices, legal action might be necessary. In this article, we’ll discuss the reasons to sue your insurer, the legal process involved, and the types of compensation you can seek.

Key Takeaways

Legal action against your own insurance company may be necessary in cases of claim denial, inadequate settlement offers, or bad faith practices.

The process of suing an insurance company involves filing a complaint, gathering evidence, and possibly proceeding to trial, often with the help of an experienced attorney.

Recoverable compensation can include economic damages (such as repair costs and other losses) and non-economic damages (such as distress) — underscoring the importance of thorough documentation.

There are several compelling reasons you might consider legal action against your own insurance company — from claim denial to insufficient settlement offers to bad-faith practices. If your insurer denies your claim, offers a settlement that doesn’t cover your losses, or engages in unethical behavior, you may need to take legal steps to recover what you’re owed.

When Your Insurance Company Denies Your Claim

Claim denials are a frustrating experience for many policyholders. Insurers may deny claims based on technicalities in the policy or the specifics of the loss. If your insurer denies your legitimate claim, it’s crucial to request a written explanation and understand your policy terms.

Legal assistance is often required to challenge a denial, especially if it seems unjustified. An experienced attorney can help file appeals and, if necessary, take the case to court to hold the insurer accountable.

Insufficient Settlement Offers

Sometimes an insurer acknowledges your claim but offers a settlement that falls short of covering your actual expenses. An insufficient offer may not adequately address repair costs or other losses you’re left paying out of pocket.

Negotiating a fair settlement — with strong documentation and, where needed, legal help — can lead to a more favorable outcome. If the insurer won’t offer a fair settlement, legal action may be necessary to reach a just result.

Bad Faith Practices by Insurance Companies

Bad faith involves insurers acting unethically or dishonestly when handling claims — such as delaying processing, failing to provide reasonable explanations for denials, or outright refusing to pay a valid claim. If you encounter such practices, consult a knowledgeable insurance attorney who can guide you through holding the insurer accountable. Legal action may be the only way to address bad faith and recover the compensation you deserve.

Suing your own insurance company involves a structured legal process that can be complex and time-consuming. It typically starts with filing a formal complaint and progresses through discovery, negotiation, and potentially trial — each step requiring meticulous documentation and, often, the expertise of an attorney.

1

Filing a Complaint

To initiate legal action, you must file a formal complaint in the appropriate court, with detailed information about the loss (date, time, location, and any witnesses). Exhaust all administrative remedies with your insurer first, and be mindful of the statute of limitations — failing to file in time can cost you the right to sue.

2

Discovery and Evidence Gathering

In discovery, both parties exchange relevant evidence. Gathering comprehensive proof — records, reports, and witness statements — is essential to building a strong case, and may include expert testimony. Adequate preparation with solid evidence can significantly impact the outcome.

Negotiation and Trial

Negotiations may lead to a settlement; if they fail, the case proceeds to trial. An experienced attorney can present your claims and negotiate for fair compensation, and — if it goes to trial — represent you in court before a judge or jury. Legal representation is crucial for navigating the complexities and maximizing your chances of success.

For a free legal consultation, call (832) 323-3000

Types of Compensation You Can Seek

When suing your own insurance company, you can seek various types of compensation to cover your losses, including economic damages like repair costs and other expenses, and non-economic damages such as distress. Understanding what’s available and how to claim it is vital to a full financial recovery.

Pain and Suffering Damages

Pain and suffering damages cover the physical and emotional distress caused by a loss. These non-economic damages can include emotional distress and a reduced quality of life. The severity of the harm and the specifics of your case determine the amount. Proving these damages is essential, and a skilled attorney can significantly improve your chances of recovering appropriate compensation.

Medical Expenses and Lost Wages

Where injuries are involved, compensation can cover medical bills, rehabilitation, and prescription costs, as well as lost income due to those injuries. Keeping detailed records of all treatment and lost income is necessary to support your claims and secure the maximum compensation available.

Property Damage and Other Costs

Property damage compensation includes costs related to:

Repairs to your property

Repair estimates from contractors

Receipts for completed repairs

Temporary living or related expenses while repairs are completed

Addressing property damage and related expenses thoroughly is crucial to maximizing your compensation.

The Role of Attorneys in Insurance Disputes

Attorneys play a crucial role in insurance disputes, helping policyholders navigate the legal system and optimize their compensation. They act as advocates in complex situations and ensure insurers are held accountable; their expertise and negotiation skills can significantly improve your chances of success.

How Attorneys Help with Insurance Claims

Attorneys help navigate the complexities of litigation and improve your chances of a favorable outcome. As skilled negotiators, they work to secure the maximum possible settlement, conduct thorough investigations, gather compelling evidence, and counter insurance adjuster arguments during negotiations.

Finding the Right Lawyer

Choosing the right lawyer involves verifying their credentials — education, training, and track record in similar cases. During the initial consultation, ask about fees and payment structure, such as contingency fees. Many firms offer free consultations to discuss your case without an immediate financial commitment.

Suing your own insurer can involve disputes, delays, and complications that hinder the process. Being aware of these potential issues helps you stay prepared and take proactive steps.

Statute of Limitations

Most states impose strict time limits on filing lawsuits against insurers, so timely action is essential. Failing to file within the designated timeframe can result in losing your right to seek compensation. An experienced attorney can help ensure you meet all legal deadlines and preserve your rights.

Insurance Coverage Limits

Policies often specify maximum payouts for different types of claims, which affects overall compensation. If damages exceed the policy’s financial caps, you could face significant out-of-pocket expenses. Understanding your policy’s limits and working with an experienced attorney can help you navigate these restrictions.

Comparative Fault Issues

Comparative fault arises when multiple parties share responsibility. If you are partially at fault, your compensation may be reduced in proportion to your share. Determining fault and liability can complicate a case and lead to disputes and delays; an experienced attorney can help navigate these complexities and advocate for fair compensation.

After deciding to sue your insurance company, take strategic steps to strengthen your case.

1

Consult an Attorney

Consulting a lawyer is vital when facing a serious loss or complex liability issues. An experienced attorney can help navigate the legal process, evaluate your case, and gather the documentation needed to support your claims. Many firms offer a free consultation to discuss your case and recommend the best course of action.

2

Initiate the Claims Process

Contact your insurer and report the loss, and notify them in writing to create a formal record of your claim. Gather all relevant documentation — reports, estimates, and policy details — to support your claim and ensure a thorough, well-documented process.

Prepare for Possible Litigation

Preparing for litigation involves filing a complaint, gathering evidence, and negotiating with the insurer. If negotiations fail, the case may proceed to trial, where your attorney represents you. Respecting the statute of limitations is crucial — missing the deadline can mean losing your right to sue.

Click to contact our property damage lawyers today

Attorney Insights: Strategies to Strengthen Your Case

From the perspective of a first-party insurance attorney, these proven tactics can make all the difference when taking legal action against your own insurer:

Send a formal notice of bad faith. Before filing suit, notify your insurer of suspected bad faith. This builds your case and may prompt faster resolution.

Request the claims file. Insist on the insurer’s full claims file, including internal notes and evaluations. These documents can uncover discrepancies that support your case.

Track all communication. Keep a dated log of every call, email, and letter. This timeline can serve as powerful evidence of delay or unfair practices.

Evaluate for punitive damages. If your state allows, explore whether the insurer’s actions rise to the level of gross misconduct — opening the door for punitive damages.

Document emotional distress. Bad faith actions often cause anxiety and disruption. With supporting documentation, these may qualify for non-economic damages.

Real-World Example

In 2020, a California policyholder sued their insurer after repeated delays and a lowball offer following a wildfire claim. With the help of an attorney, they secured a $3.1 million jury verdict — more than six times the original offer — after proving the insurer acted in bad faith by failing to investigate properly and delaying payment for over a year.

Case Law Spotlight

In Gruenberg v. Aetna Insurance Co., 9 Cal.3d 566 (1973), the California Supreme Court established that an insurer’s duty of good faith is independent of the contract itself. When breached, it gives rise to a tort action, allowing claimants to recover damages beyond the policy limits, including emotional distress and punitive damages.

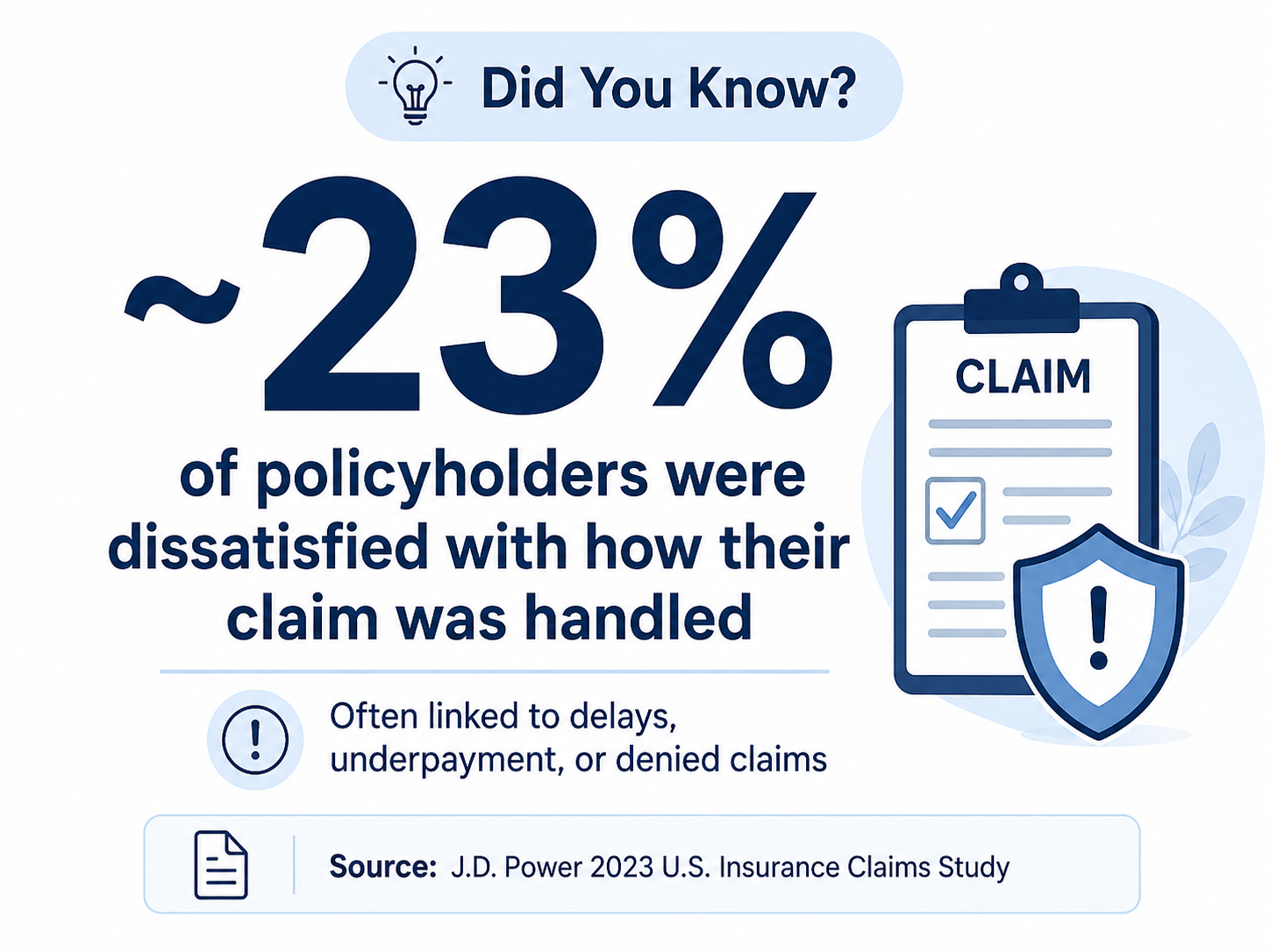

Did You Know?

According to a 2023 J.D. Power U.S. Insurance Claims Study, nearly 23% of policyholders who filed a claim for auto or property damage reported dissatisfaction with the insurer’s handling — often due to delays, underpayment, or denied claims. Many of these cases lead to legal action when bad faith is suspected.

Complete a Free Case Evaluation form now

Summary

Suing your own insurance company can be daunting, but understanding the reasons behind such lawsuits, the legal process involved, and the types of compensation you can seek is crucial. Experienced attorneys play an essential role in navigating these disputes and advocating for fair compensation. By staying informed and taking proactive steps, you can hold your insurer accountable and pursue the financial recovery you deserve. Remember, timely action and thorough preparation are key to a successful outcome.

Frequently Asked Questions

What are the common reasons for suing your own insurance company?

Common reasons include claim denial, insufficient settlement offers, and the insurer’s bad-faith practices. Understanding these factors can help you determine if legal action is warranted.

How do I start the legal process against my insurance company?

You should file a formal complaint in court. That is followed by discovery, negotiation, and possibly a trial if no resolution is reached.

What types of compensation can I seek in a lawsuit against my insurance company?

You can seek compensation for property damage, repair costs, and other losses, as well as non-economic damages such as distress, where applicable. Gather comprehensive documentation to support your claims.

How can an attorney help with my insurance claim?

An attorney can navigate legal complexities, negotiate settlements, gather crucial evidence, and represent you in court if needed — ultimately leading to a more favorable outcome.

What challenges might I face when suing my own insurance company?

You may face challenges such as the statute of limitations, insurance coverage limits, and comparative fault issues. These complexities can significantly impact the outcome of your case.

Call or text (832) 323-3000 or complete a Free Case Evaluation form