Climate Change Means Getting Insurance Coverage Is Increasingly Difficult – Especially In Some States

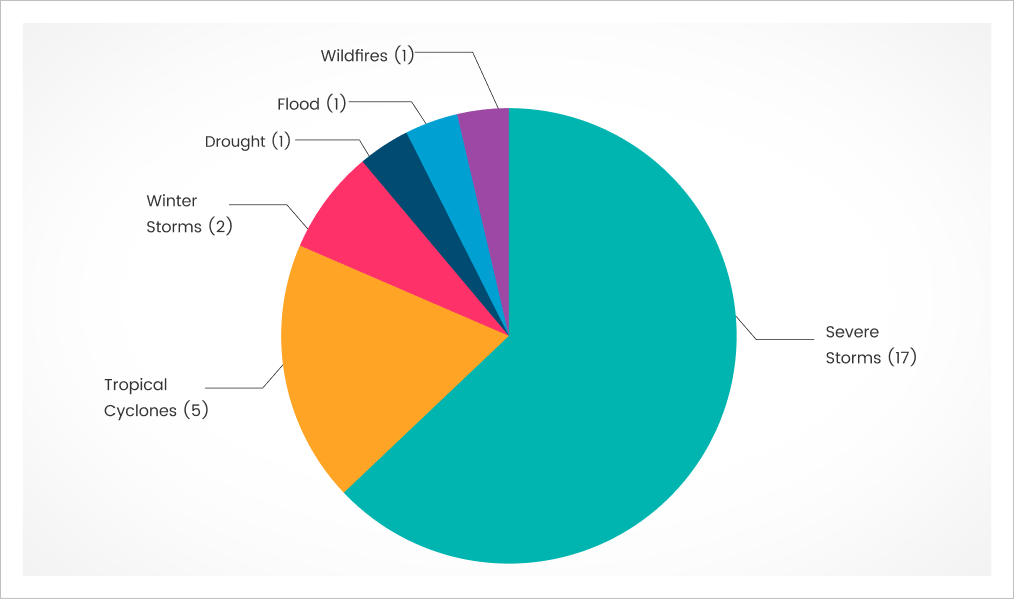

The worsening effects of climate change are impossible to ignore. According to the 2024 NOAA climate study, the U.S. experienced 27 major disasters, causing hundreds of billions of dollars in damage nationwide. These devastating weather events included droughts, flooding, severe storms, tropical cyclones, wildfires and winter storms, with data suggesting an increase of similar events in the future.

Our study takes a look into the worst-hit areas, and how the continuing volatility around climate-related events is affecting insurance premiums, with homeowners facing an increasing struggle to put protective indemnities in place to safeguard their property investments and financial stability.

Key Climate Disaster Events

In 2024, several devastating climate-related events made headlines, including:

Hurricane Helen struck from September 24 to 29, sweeping across parts of Florida (from Big Bend to St. Petersburg), Georgia, western North Carolina, southwestern Virginia, and eastern Tennessee. The storm caused an estimated $79.6 billion in damages.

Hurricane Milton hit on October 9 and 10, resulting in the deaths of 32 people and causing $34.3 billion in damages.

Hurricane Beryl made landfall in Texas on July 8, affecting western Louisiana and Arkansas as well. It claimed 46 lives and caused about $7.2 billion in damages.

A powerful tornado outbreak swept through Florida, Alabama, Tennessee, and the Carolinas between May 6 and 9. It killed three people and left behind $6.6 billion in damage.

2024 Billion-Dollar Weather & Climate Disasters

An analysis of the study data shows that, since 1980, many states have spent enormous amounts responding to the destruction caused by climate-related disasters. Since 1980, Florida has spent more than any other U.S. state on weather-related disaster recovery, a staggering $450 billion, primarily due to hurricane damage. Texas follows closely with $436 billion in costs, but it tops the list in terms of the number of separate billion-dollar disasters, with 190 major events recorded through 2024. Louisiana ranks third, having incurred $314 billion in damages from several large-scale disasters.

Below are the top ten states with the highest rebuilding costs from climate-related events since 1980.

From 2021 to 2024, annual insurance premiums for a typical U.S. homeowner increased by an average of $648, a 24 percent increase – far higher than the 11 percent cumulative inflation increase over the same period.

During this timeframe, insurance premiums rose in 95% of U.S. zip codes, with one in three policyholders facing rate hikes exceeding 30%. While inflation played a role, the primary driver behind most of these increases was the growing frequency and severity of climate-related disasters.

While the U.S. has seen an average insurance premium increase of 24%, the impact has varied widely by state and city, some areas have been hit much harder than others, and rates are projected to climb even higher by the end of 2025. The sharp disparity in premium increases due to climate disasters is clear when looking at the cities most affected: all 10 of the U.S. cities projected to have the highest home insurance costs in 2025 are located in Florida or Louisiana. Leading the list is Hialeah, Florida, where homeowners are expected to pay an average premium of $16,693, over 7.5 times the national average.

Let’s consider some key area changes, and the level of further projected rises.

Florida

Statewide Floridian home insurance premiums already average $9,462 per year due to the prevalence of hurricanes and due to many insurance companies refusing to offer coverage in the area (circumstances that leave many homeowners needing to rely on state-backed insurance coverage). By the end of 2025, Florida is projected to see the most expensive annual premiums in the country, with homeowners stumping up an average $15,460.

Louisiana

Premiums surged in Louisiana in 2024, reaching a peak average rate of $10,964, largely due to various instances of hurricane damage and hefty insurer losses – a factor that made insurance coverage difficult to arrange. For those in Louisiana who can get it, home insurance coverage is projected to cost $13,937 by the end of 2025 – a swingeing 27% increase.

Oklahoma

Oklahoma home insurance premiums soared to $7,762 in 2024, driven by tornadoes, hail, and severe winds. Hikes are also in part due to insurers unwilling to offer policies, with many refusing to renew existing arrangements. For example, Oklahoma Farmers Insurance, the state’s second-largest home insurance company, announced last year that it would not renew 1,300 policies due to wildfire risk.

By the end of 2025, Oklahoma residents can expect premiums to hit $8,639. Little wonder with ongoing trends: between 2022 and 2023, the state suffered a 41% increase in tornadoes.

Colorado

In Colorado in 2024, home insurance premiums rose 11% to $5,984, largely due to hail damage. Insurers continue to adjust risk models on an ongoing basis, which will make coverage harder to secure in future; those who are successful can expect an 11% increase, to an average $6,630 fee. No real surprise when we consider the fact that, in 2023, Centennial State insurers lost money – paying out more in claims than they took from premium contributions.

Texas

Home insurance premiums for Texans rose to $6,005 in 2024 (set to rise by 9% to $6,522 in 2025), with hurricane and flood risk behind increasing costs. Many insurers stopped writing policies for Gulf Coast homeowners in 2024 due to the rising damage risk in the area. In the wake of Hurricane Beryl, Progressive Insurance sent out non-renewal notices to homeowners in the area, citing “risks relating to natural and catastrophic losses”.

Alabama

In Alabama, more than 400 twisters have struck over the last five years, causing more than $34 million dollars of property damage. The financial consequences don’t end there: 2024 homeowner insurance premiums of $5,445 are set to rise 7% to $5,831.

Nebraska

According to NOAA data, Nebraska endured 63 tornadoes in 2023, which represented a 142% increase on 2022 figures. The Cornhusker State has the third-highest expected losses from hail in the U.S., with Douglas County in particular considered by FEMA to be “very high risk” for hail damage. As such, non-renewal rates have increased, with homeowners struggling to find insurers: 2024 premiums of $4,725 will see a 10% rise to $5,203 through 2025.

Mississippi

In 2020, Hurricane Zeta battered 10,000 homes, causing $635 million in losses; the rising cost of reinsurance has also put a squeeze on home insurance rates, with insurers paying out more in claims than they collected in premiums. The unsurprising result is that the average annual cost of home insurance in Mississippi in 2024 was $4,809, which is set to rise another 8% in 2025, to $5,198.

Arkansas

May 2024 saw 110 tornadoes hit Arkansas, the resulting damages costing $3.5 billion. Arkansan catastrophic misfortune continued as another 10 tornadoes struck on July 8, marking the largest tornado outbreak on record for the beleaguered state during that particular month. FEMA data suggests that Arkansas remains at “very high risk” of likely devastating ice storms, which compounds growing home insurance premium rates. In 2022 and 2023, Arkansas insurers paid out more than they collected; 2024 average home insurance rates of $4,490 are set to rise 13% in 2025, to $5,077.

Kansas

The average annual cost of homeowner insurance in the Sunflower State in 2024 was $4,556, but by the end of 2025 that’ll look more like $4,782 due to a projected 5% increase. Kansas suffered 45 tornadoes in 2023, with preliminary reports suggesting 89 tornadoes in total struck in 2024, and recorded the second highest number of severe wind events (948) of any state in 2024, according to National Oceanic and Atmospheric Administration (NOAA) data. Additionally, hail continues to be a major concern, with hail-related events increasing 68% between 2022 and 2023; Kansas dealt with 778 separate hail events during the latter year.

The following are the main environmental factors that have caused the biggest spikes in insurance premium costs, according to Brookings Institution and NOAA data:

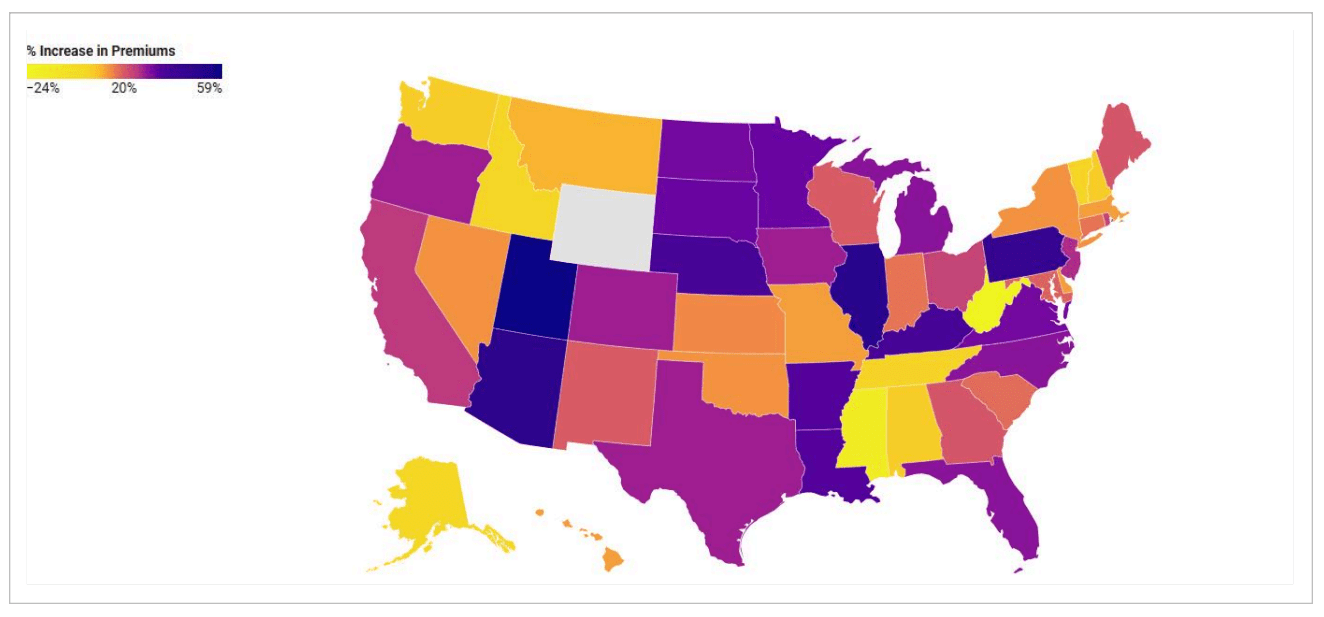

States Set To Suffer The Biggest Home Insurance Rises in 2025

Homeowners across every U.S. state can expect their insurance premiums to rise in 2025, with increases ranging from 2% to as much as 27%. For those on the higher end, these hikes represent steep jumps to staggering costs. States like California, Iowa, Hawaii, and Louisiana are set to see rate increases more than twice the national average of 8%. Here’s a look at the states hit hardest and some contributing factors for the predicted increases.

Louisiana

Louisiana homeowners are set to suffer a 27% insurance hike in 2025, pushing the average rate to $13,937. This is actually a decrease in percentage rises: in 2024, the state saw insurance premiums rise by a staggering 38%.

California

Two of the three worst fires in California’s history devastated Los Angeles County in January 2025, with total losses estimated by UCLA at around $131 billion, including $45 billion in insured losses. Many insurers have stopped writing new policies, forcing homeowners into expensive alternatives. Of those still offering insurance, in February 2025 California State Farm requested an emergency 22% rate hike due to wildfires; in March, the CDI “provisionally” granted the increase. (Interestingly, California regulators fined multiple insurers over unfair claim denials following the wildfires, forcing them to reassess thousands of rejected claims.) For 2025, a 21% increase is expected, taking average rates to $2,930 (this after a 10% increase in 2024).

Iowa

A projected 19% home insurance increase for Iowans will push their average rates up from $3201 to $3825, with hail, flooding, and strong winds major contributory factors. Iowa recorded 131 tornadoes in 2024, the second most of any state, and between 2022 and 2023, hail events in the state increased by 133%. Insurers have responded to the growing risk of roof damage by shifting from using replacement value coverage to using actual cash value coverage, further putting the onus on homeowners by factoring in depreciation when paying out claims.

Hawaii

Hawaiians can expect a 17% increase by the end of 2025, taking premiums up from $1548 to $1808. In 2023, America’s deadliest wildfire in over 100 years devastated parts of Hawaii, causing 102 deaths and damaging thousands of homes, leading to $3 billion in insured losses, with insurers paying out $389 for every $100 paid in.

Minnesota

In 2025, Minnesota homeowners will see a 15% increase in policy rates, with the average premium rising from $3,524 to $4,058. After years of heavy losses from a steady stream of disaster-related claims, insurers have had little choice but to pass the cost on to policyholders. Throughout the 2010s, Minnesota averaged one billion-dollar disaster per year, but in just the past three years, the state has been hit by 18 separate billion-dollar events. If you’re looking for clear evidence that climate disasters are accelerating, Minnesota makes a compelling case.

North Carolina

North Carolina is expected to see a 7.5% average increase in home insurance premiums starting June 1, 2025, with another 7.5% hike set for June 1, 2026. Contributing to these rising costs are increasing climate risks, including the threat of hurricanes, like Hurricane Helene, which highlighted the state’s growing vulnerability to severe storm damage.

Rising Cost of Homeowners Insurance: 2021–2024

Projected Rises Vs Actual Rises, With Projections Often Too Conservative

As part of this study, we’ve offered a series of projected hikes, but the reality is often much steeper. Here’s a perfect illustration of that particular phenomenon.

| # | State | 2023 Premium Rate | 2024 Predicted Premium Rate | 2024 Actual Premium Rate |

|---|---|---|---|---|

| 1 | Florida | $10,996 | $11,759 | $14,140 |

| 2 | Louisiana | $6,354 | $7,809 | $10,964 |

| 3 | Oklahoma | $5,444 | $5,711 | $7,762 |

| 4 | Texas | $4,456 | $4,437 | $6,005 |

| 5 | Mississippi | $4,312 | $4,482 | $4,809 |

| 6 | Colorado | $4,072 | $4,367 | $5,984 |

| 7 | Nebraska | $3,962 | $4,292 | $4,725 |

| 8 | Alabama | $3,939 | $4,281 | $5,445 |

| 9 | Kansas | $3,437 | $3,666 | $4,556 |

| 10 | Arkansas | $3,368 | $3,662 | $4,490 |

Study data confirms that actual 2024 home insurance rates significantly outpaced initial projections. Florida shows the largest differential between actual 2024 rates ($14,140) and projections ($11,759), with a wide gap between Texas’ 2024 actual rate ($6,005) and the projection ($4,437). There are multiple reasons for the rise beyond the increasing weather events: rising material costs and regulatory changes are also key factors.

1. Additional Reasons For Homeowner Premium Increases

✓

Five of the eight most expensive states for home insurance are situated along the vulnerable Gulf Coast. The region is extremely susceptible to hurricanes, which cause more financial damage than any other type of natural disaster.

✓

Labor shortages in the construction industry have played a major role in driving up insurance premiums in recent years. As of August 2024, there were 368,000 open construction jobs in the U.S., more than twice the number forecasted by the Bureau of Labor Statistics. This workforce gap drives up rebuilding costs and claim payouts, which in turn pushes premiums higher for homeowners across the board.

✓

Inflation has only made matters worse, contributing to surging material prices and ongoing supply chain disruptions.

✓

Even first-time claimants aren’t immune. In states hit by catastrophic events, a single large claim can still trigger premium increases of 7% to 10%.

2. Some Ways To Reduce Your Homeowner’s Insurance

Apart from moving to a state offering low insurance premiums, there are measures you can take to reduce your rates. These include increasing your deductible, bundling your coverage, applying any available discounts, making weather-resistant updates to your property, improving your credit rating, and removing any inessential coverages. By working with an independent insurance agent, you can make sure you get the very best available premium rate.

3. Legal Recourse And Litigation Trends

✓

Homeowners looking to take legal action over denied insurance claims often face a maze of regulatory challenges, as consumer protections differ drastically from state to state. Policyholder rights, coverage guarantees, and options for financial recovery vary widely, leaving some homeowners far more vulnerable than others. While certain states enforce strict claim review standards, others give insurers greater leeway to reduce or deny payouts with minimal oversight.

✓

Lawsuits against insurers are becoming more common as homeowners push back against unfair practices, but many still struggle to access the legal support needed to pursue the compensation they deserve.

Here are a few notable examples of consumer action taken in response.

Breach of Contract Lawsuits

Homeowners frequently sue insurers for failing to honor policy terms. These cases often rest on the argument that the insurer wrongfully denied a claim, despite clear coverage provisions.

In the case of Kazi Ahmed v. Hamilton Insurance DAC, the Florida homeowner sued the insurer after a Hurricane Irma-related claim was denied, alleging the company misinterpreted policy exclusions to avoid payout.

Bad Faith Insurance Litigation

Some lawsuits allege that an insurer has acted unreasonably in denying or delaying claims, and by doing so violating their duty to policyholders.

In the case of Jerome Gruenberg v. Aetna Insurance Company, the California homeowner won a bad faith lawsuit after proving their insurer intentionally delayed processing a storm damage claim, which subsequently caused financial hardship. The court held that an insurer’s delay in processing claims can constitute bad faith if it lacks a reasonable basis. Plaintiffs often reference this case when arguing that insurers wrongfully delay payments after major events like wildfires.

Class Action Lawsuits Against Insurers

A collective group of policyholders may file class action suits against insurers for broad claim denials or deceptive practices.

A national class action lawsuit (Bottega, LLC v. National Surety Corporation) targeted an insurer for systematically underpaying claims related to wildfire damage, arguing that the company used flawed valuation methods.

Other significant examples of consumer lawsuits against insurers include:

Over 50,000 Florida insurance claim denials regarding Hurricane Helen

A Florida insurance company fined $100,000 over Hurricane Ian claims

A California homeowner who sued insurers over wildfire coverage denials

The California FAIR Plan faced a lawsuit over denied wildfire claims, with homeowners accusing the FAIR Plan of bad faith after being underpaid or denied coverage regarding smoke damage.

Study data reveals that these are the ten insurance companies with the highest likelihood of denying disaster-related claims:

By 2035, the U.S. is expected to face even more drastic shifts in climate, including a sharp rise in destructive weather events. This creates a daunting road ahead for both insurers and homeowners, one where the financial fallout may be even harder to predict than the climate trends themselves.

Methodology

For all 2024 data tables, rates in this report represent the average annual cost of an HO-3 insurance policy for homeowners with a good credit rating and zero claims made over the previous five years. The average example cost refers to a single-family frame house with the following coverage limits: $400,000 dwelling, $25,000 personal property, $30,000 loss of use, $300,000 liability, and a $1,000 deductible.

For the 2024 rate prediction data set, we referred to Insurify.com data included in a 2023 report on home insurance affordability and compared the numbers to the actual 2024 premium rates.