Can You Sue an Insurance Company for Denying Your Claim?

Was your insurance claim denied unfairly? Suing an insurance company for denying a claim might be necessary. In this guide, discover why claims are denied, how to identify bad faith actions, and the legal steps you can take to challenge the denial.

For a free legal consultation, call (832) 323-3000

Key Takeaways

✓

Insurance companies must act in good faith, and if a valid claim is denied, that denial may indicate bad faith, allowing policyholders to challenge it.

✓

After a claim denial, it’s essential to gather additional evidence, review denial notices, and request reconsideration to improve the chances of a successful appeal.

✓

Consulting an attorney can significantly aid in navigating bad-faith claims, ensuring that all legal rights are preserved and maximizing the potential recovery of damages.

Understanding Claim Denials

Insurance companies often deny claims to save money. Often, this isn’t because your claim lacks merit but because the insurer hopes you’ll accept the denial without a fight. Insurers are legally required to act in good faith and deal fairly with their policyholders. This means they must pay benefits when a valid claim meets the conditions outlined in the policy. When an insurer denies a legitimate claim, they may be acting in bad faith, and you have the right to challenge this.

In Massachusetts, insurance companies have a legal obligation to act in good faith. They must also adhere to the terms outlined in their contracts with policyholders and fulfill their contractual obligations. Failing to do so can place claimants in precarious situations, potentially leading to significant financial and emotional stress.

Recognizing the reasons behind your claim denial and identifying bad-faith actions are crucial to resolving the situation.

Real-World Example

In 2023, a homeowner in Massachusetts successfully challenged their insurer in court after a $75,000 property damage claim was denied due to an alleged lapse in coverage. The court found that the insurer failed to properly communicate the policy renewal terms, resulting in a judgment in favor of the homeowner. This real-world case underscores the importance of understanding policy language and the insurer’s obligations.

Common Reasons for Claim Denials

Insurance claims can be denied for several valid reasons. Commonly, these include policy exclusions, where the event causing the loss isn’t covered by your policy, and insufficient evidence to support the claim. For example, if you file a claim for water damage but fail to provide adequate proof of the damage or its cause, the insurance company may rightfully deny it. Knowing these valid reasons helps differentiate between a justified denial and one made in bad faith.

However, not all denials are justified. Sometimes insurers use vague policy language or interpret the terms in their favor, resulting in an unreasonable denial. Knowing the common reasons for denials can help you counter these tactics. A denial without a valid reason may indicate bad-faith actions by your insurer.

Identifying Bad Faith Actions

Bad faith from an insurance company involves engaging in dishonest practices. This can take many forms, such as delaying payments, unjustly denying claims without legitimate reasons, and misrepresenting policy terms. For instance, if your insurer unjustly delays your payout or mishandles your claim, they may be acting in bad faith.

Documenting all communications with the insurer after a denial is essential. Keep records of emails, letters, and phone calls, as these can serve as evidence if you need to prove bad faith actions. Meticulous documentation and understanding bad faith actions help protect your rights and strengthen your case against the insurer.

If your insurance claim has been denied, it’s important to act quickly. Here are some steps to consider:

1

Build a strong case by gathering all relevant documentation.

2

Consult with an attorney for valuable guidance on navigating the complexities of the appeal process effectively.

3

Avoid unnecessary stress or missed deadlines by staying organized and proactive.

If you believe the denial is unjust, following specific appeal steps is crucial.

Reviewing the Denial Notice

The first step after receiving a denial notice is to review it thoroughly. The notice should outline the specific reasons for the denial and reference relevant policy language. Knowing these reasons is vital for crafting an effective response. If the denial is based on a misunderstanding or an oversight, addressing it promptly can sometimes resolve the issue without further conflict.

Gathering Additional Evidence

Insurance companies may deny claims due to inadequate documentation or failure to follow procedures. Gathering new documentation to support your original claim is crucial. This might include photographs, repair estimates, medical records, or witness statements.

Additional evidence strengthens your case and improves the chances of a favorable outcome.

Requesting a Reconsideration

Once you have reviewed the denial notice and gathered additional evidence, the next step is to request a reconsideration. The denial notice should clearly outline the procedures to appeal the decision. Adhering meticulously to these procedures is crucial. Write a formal letter outlining why the initial decision was wrong and include any new evidence that supports your claim.

A compelling appeal, accompanied by all necessary documents, can increase the insurer’s chances of reconsidering their decision. A well-prepared appeal demonstrates that you are serious about your claim and willing to fight for the compensation you deserve.

If your claim is unjustly denied, you have the right to sue the insurance company. Legal grounds for suing an insurance company include breach of contract and bad faith actions. In Massachusetts, victims can file a lawsuit for greater damages if their initial claim is denied. When an insurer denies a legitimate claim without a valid reason, they can be held legally responsible.

Although challenging a denial or pursuing legal action can be daunting, it is often necessary for fair treatment. Consulting with an attorney can help determine if you have a strong case and guide you through the legal process.

Consider legal action if the insurer acts in bad faith or significantly delays or mishandles your claim, leading to an unreasonable delay.

Relevant Case Law

One landmark case illustrating bad faith practices is Zielinski v. Massachusetts Insurers Insolvency Fund, 464 Mass. 590 (2013). The Massachusetts Supreme Judicial Court held that insurers must conduct a prompt and fair investigation of claims. Failure to do so can expose them to liability for bad faith under state consumer protection laws.

Consulting with an Attorney

If you believe your insurer is acting in bad faith, consulting with a knowledgeable insurance attorney is crucial. An experienced lawyer can offer options, whether to sue or seek mediation. They can help identify valid claims supporting legal action and navigate legal complexities.

Hiring an attorney before filing a lawsuit can greatly increase your chances of recovering higher compensation. Many clients have successfully recovered damages after facing denial from their insurers thanks to effective legal representation.

A free consultation can clarify your rights and the best course of action.

Filing a Lawsuit Against the Insurer

Filing a lawsuit for bad faith begins with sending a demand letter to the insurer. If the insurer doesn’t settle, further action is necessary. The next step involves filing a formal complaint in court. This initiates the lawsuit process and requires the insurer to respond to the allegations.

During the discovery phase, both parties collect and share evidence relevant to the case. This phase is essential for building a strong case against the insurer. The goal is to demonstrate that the insurer acted in bad faith and to seek compensation for the denied claim. An experienced attorney can guide you through each step, ensuring that all legal procedures are followed.

Click to contact our property damage lawyers today

Proving Bad Faith in Court

It is a challenging task to prove that the insurer acted in bad faith. This process requires substantial evidence and careful consideration. To establish a bad faith claim, you need evidence of dishonest or unfair actions by the insurer. This includes demonstrating that the insurer’s actions deviated from accepted industry standards. Effectively collecting and presenting this evidence is crucial for a successful outcome.

Proving that an insurer acted in bad faith requires substantial evidence that its conduct was dishonest or unreasonable and deviated from accepted industry standards. Courts look for a pattern of unfair claim handling — unjustified delays, inadequate investigation, or denials without a reasonable basis — so organizing and presenting that evidence clearly is essential to a successful claim.

Types of Evidence Required

Evidence showing an insurer’s dishonesty or unfairness is crucial to demonstrating bad faith. Legal professionals can organize and present evidence of deceptive practices compellingly to strengthen their case. Successful outcomes often involve challenging insurers who acted in bad faith during the claims process.

The Role of Expert Witnesses

Expert witnesses can provide insights into industry standards and assess whether the insurer deviated from those norms. Their testimony can clarify deviations from standard practices that indicate bad faith. Engaging expert witnesses can greatly strengthen your case by offering an authoritative perspective on the insurer’s actions.

Complete a Free Case Evaluation form now

Potential Damages You Can Recover

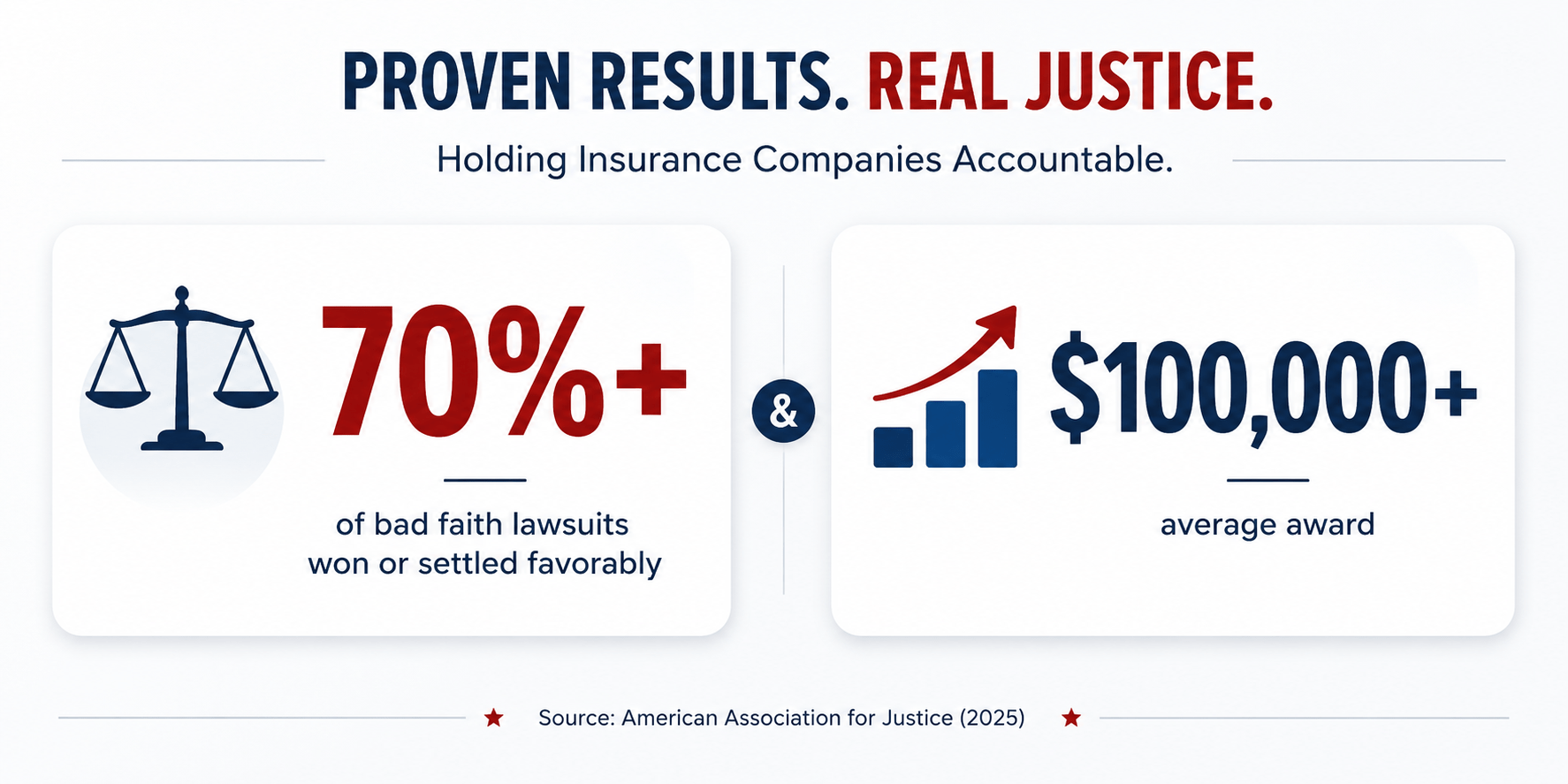

Pertinent Statistic

According to a 2022 study by the American Association for Justice, policyholders win or settle favorably in over 70% of bad faith insurance lawsuits, with the average award exceeding $100,000. This demonstrates the strong legal protections available to consumers and the potential value of pursuing a claim.

Recoverable damages in bad-faith lawsuits include contract, extracontractual, and punitive damages. These damages can cover unpaid claims, medical bills, repair costs, and more. There is no cap on the amount you can sue an insurance company for, which means the compensation can be substantial. The types of damages you can claim are influenced by the type of policy and the losses suffered, including property damage. If the insurer violates the Unfair and Deceptive Trade Practice Act, the court may award triple damages and attorney’s fees.

Compensatory Damages

Compensatory damages cover actual losses, such as medical expenses and property damages from a claim denial. Hiring an attorney can greatly enhance your chances of a successful outcome in insurance lawsuits. These damages are designed to make you whole again by covering the financial impact of the denied claim.

Punitive Damages

Punitive damages can be awarded in bad-faith cases, though rarely. The court may order punitive damages for the insurer’s intentional misconduct. These damages serve to penalize insurers for particularly wrongful actions and require a higher standard of proof. The purpose is to punish the insurer and discourage future bad faith behavior.

Time Limits for Filing a Lawsuit

In North Carolina, a claimant has 3 years from the date of the incident to file a bad-faith insurance lawsuit. The statute of limitations begins when the insurance company’s wrongful act occurs, not when the insurance policy is purchased.

Missing the deadline to pursue a bad-faith claim against an insurance company can result in losing the right to seek legal recourse.

Importance of Acting Quickly

Timely action after a claim denial ensures all legal rights are preserved, and deadlines are met. Missing the deadline to file a bad-faith claim can result in the loss of the right to legal recourse. Acting quickly ensures you do not forfeit your right to compensation.

At Storm Law Partners, we understand the complexities of navigating insurance claim denials. Our attorneys possess extensive knowledge of insurance policies and legal strategies. We prepare appeals, gather evidence, and advocate for clients to secure the compensation they deserve.

You have rights, and our firm is dedicated to protecting them.

Services Offered by Our Lawyers

Our lawyers offer comprehensive services for clients, from evaluating the viability of a claim to gathering necessary evidence and providing legal counsel and courtroom representation. These services combined enhance the likelihood of a successful outcome.

Success Stories

Our firm has successfully represented numerous clients who faced wrongful denials of claims by their insurance providers, including cases in which an insurer’s denial led to significant financial distress. For instance, we secured a six-figure settlement for a family whose claim was improperly denied due to an alleged policy exclusion.

These cases exemplify our commitment to fighting for policyholders’ rights and ensuring fair compensation.

Summary

Additional Attorney Insights

✓

Always request a certified copy of your entire insurance policy to better understand your coverage.

✓

Document every interaction with your insurer, including dates, names, and content of conversations.

✓

File complaints with your state’s Division of Insurance if the insurer violates regulations.

✓

Consider early mediation as a strategic move before resorting to litigation.

✓

Look for patterns of systemic denial, which may suggest broader misconduct—something courts take seriously.

Understanding your rights when dealing with an insurance claim denial is crucial. From recognizing valid reasons for denial to identifying bad-faith actions, knowing the steps to take can make a significant difference in the outcome. Acting quickly, gathering additional evidence, and consulting with an attorney are vital steps in challenging a denial. If necessary, pursuing legal action can help you recover compensatory and punitive damages. Remember, timely action and proper legal guidance can ensure you receive the compensation you deserve. Don’t let an insurance company’s unjust denial stand in the way of your rightful claims.

Frequently Asked Questions

What are common reasons for insurance claim denials?

Insurance claims are often denied due to policy exclusions, insufficient evidence, and inadequate documentation. Ensuring thorough documentation can help mitigate these issues.

How can I identify if my insurer is acting in bad faith?

You can identify whether your insurer is acting in bad faith by recognizing unreasonable claim denials, excessive processing delays, or mishandling of claims. Maintaining thorough documentation of all communications and identifying unjust denials can be crucial indicators of bad-faith practices.

What steps should I take after my insurance claim is denied?

If your insurance claim is denied, carefully review the denial notice for specific reasons, then gather any additional evidence to support your claim. Submit a formal letter requesting reconsideration along with the new evidence.

When should I consider suing an insurance company?

Consider suing an insurance company if your claim is unjustly denied and you suspect bad faith or breach of contract on their part. Consulting an attorney can clarify your case’s strength and options.

What types of damages can I recover in a bad-faith lawsuit?

In a bad-faith lawsuit, you can recover compensatory damages for actual losses, such as medical expenses and property damage, as well as potential punitive damages to punish the insurer’s misconduct. This combination helps ensure accountability and discourages similar behavior in the future.

Call or text (832) 323-3000 or complete a Free Case Evaluation form