Does home insurance cover water damage? Yes, but with conditions. In this guide, we’ll break down which types of water damage your homeowners’ insurance likely covers, and which situations might leave you uncovered, so you know exactly how your policy protects you.

Key Takeaways

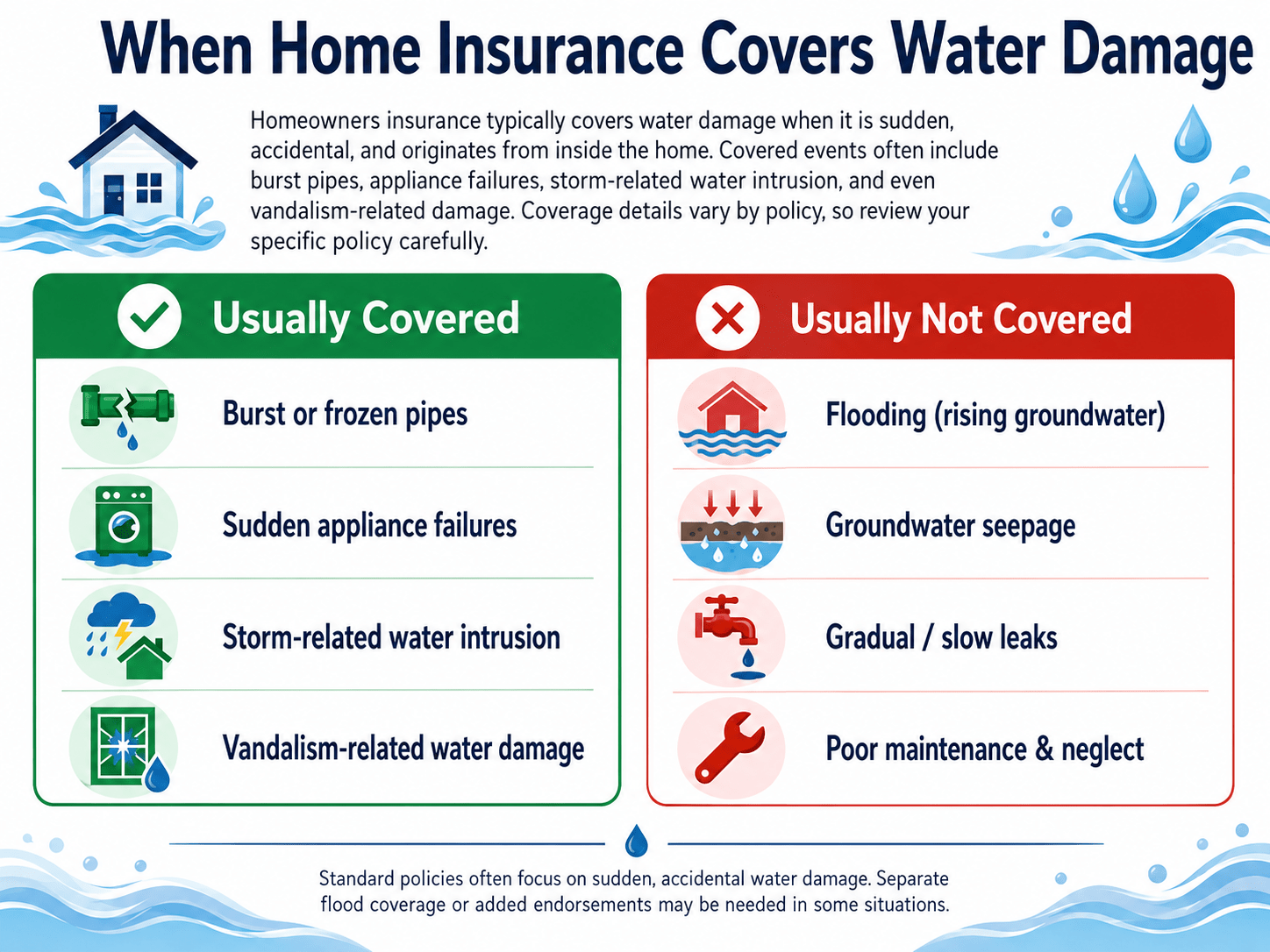

Homeowners insurance typically covers sudden and accidental water damage from events such as burst pipes or appliance failures, but excludes damage from floods and poor maintenance.

To enhance protection, homeowners can consider optional coverages like sewer backup and mold remediation, which are not included in standard policies.

Proper maintenance and routine inspections of plumbing and appliances are essential to prevent water damage, since neglect can lead to coverage exclusions.

Homeowners insurance typically covers water damage if it’s sudden or accidental and originates from inside the home. Events like a burst pipe or storm-related water intrusion are generally covered under standard policies, which are designed to protect you from unexpected incidents and help repair the damage.

Coverage can also extend to scenarios like water damage caused by vandalism. The specifics vary by insurer and policy, so it’s always wise to review your own policy.

Sudden and Accidental Events

Homeowners insurance generally covers water damage caused by sudden and accidental events. A burst pipe is a prime example, as are pipes that freeze and subsequently burst. These occurrences are unexpected and beyond the homeowner’s control, which is why they are covered.

However, damage that occurs gradually or due to poor maintenance may not be covered. You can expect your policy to step in for sudden, unforeseen incidents, but liability for ongoing issues often remains with the homeowner.

Coverage for Appliance Failures

Water damage resulting from sudden appliance failures is typically covered. For example, if a water heater malfunctions and causes significant water damage, the incident would generally be covered. Note that while the resulting damage may be covered, the cost of repairing or replacing the appliance itself often is not — so review your policy to understand what’s included and whether extra coverage is necessary.

While homeowners’ insurance covers many types of water damage, there are notable exclusions. The biggest is flood damage — water entering the home from the ground — which requires a separate flood insurance policy. Other common exclusions include groundwater seepage, gradual leaks, and damage from unresolved maintenance issues.

Gradual Damage and Poor Maintenance

Insurance does not cover water damage from poorly maintained plumbing or appliances. For example, if a homeowner neglects a leaky toilet or dripping faucet, the resulting damage typically isn’t covered. Ignoring small issues can lead to significant problems over time, which insurers view as preventable, so regular inspection and maintenance are essential to avoid non-covered water damage.

Flooding Exclusions

Standard homeowners’ insurance does not cover flood damage. Flooding water inundating normally dry land or multiple properties is specifically excluded, so you must purchase a separate flood insurance policy (available through the National Flood Insurance Program), which can be crucial in flood-prone areas. Knowing the distinction between covered water damage and flood damage helps you make informed decisions and avoid being caught off guard.

For a free legal consultation, call (832) 323-3000

Optional Water Damage Coverages

To enhance protection, homeowners can purchase extra coverage beyond a standard policy. These optional coverages can be invaluable for protecting against specific types of water damage that are otherwise excluded.

Sewer and Drain Backup

Sewer backup insurance is an optional add-on that covers damage from backed-up sewage — crucial for protecting against claims from overtaxed sump pumps and backed-up sewer lines. It typically includes the cost of repairing damaged sewer lines, cleaning up sewage, and possibly temporary accommodations if the home becomes uninhabitable. It’s especially important for homes with a basement, where sewer backups can cause significant damage.

Mold Remediation

Homeowners can include mold coverage to guard against unexpected mold damage and address hidden mold growth that may not be immediately visible. This matters because mold can develop quickly after water damage and can be costly to remediate. Given the potential health risks and property damage, this optional coverage is a wise investment.

Filing a water damage claim involves a few crucial steps to ensure the damage is documented and the claim is processed efficiently.

1

Immediate Steps After Damage Occurs

Determine the water source and stop the flow to prevent further issues, then take photographs of the damage and any affected items for your claim. Prompt reporting is vital, as mold and mildew can develop within 24–48 hours. If the damage is extensive, contact a water-damage restoration company to handle cleanup and drying.

Working with Adjusters

Adjusters evaluate the damage, determine coverage, take photos and measurements, and assess whether the damage was sudden or preventable. Collaborate with your contractor and the adjuster on repair costs, and consider engaging an independent insurance agent to help negotiate. This cooperation ensures efficient repairs and appropriate financial assistance.

Preventing Water Damage

Preventing water damage is always better than dealing with the aftermath. Routine plumbing inspections can catch hidden leaks before they escalate, and regular gutter cleaning helps prevent water from pooling and causing foundation damage.

Regular Maintenance

Regular maintenance of plumbing and appliances is crucial. Routinely check for leaks and ensure appliances like water heaters are in good working condition. Adding an optional mold endorsement can provide extra protection against mold from water leaks. Staying proactive prevents small issues from becoming major problems — protecting your property and saving on repairs and claims.

Seasonal Preparations

Disconnect outdoor hoses to prevent freezing, clean gutters and downspouts before winter to prevent ice build-up, and inspect and seal cracks in windows and doors to reduce water intrusion during storms. Winterizing pipes and preparing for seasonal changes significantly reduces the risk of burst pipes and water damage year-round.

Click to contact our property damage lawyers today

Understanding Your Policy Terms

Examine your policy for specific clauses that define the limitations of water damage coverage. Policies often include sublimits, which can significantly reduce water damage coverage compared to your total property coverage. Understanding your coverage limits and deductibles is crucial, as these factors significantly impact water damage claims.

Familiarize yourself with your policy to determine which types of water damage are covered and under what circumstances. Adding optional coverages can enhance protection, and being well-informed about your policy terms ensures you’re adequately prepared for any eventuality.

If the insurer still won’t reconsider despite a well-documented appeal, you can file a complaint with your state department of insurance, which oversees insurer conduct and can press for a fair review.

Complete a Free Case Evaluation form now

Attorney Insights: Strengthening Water Damage Claims

As a first-party property insurance attorney, here are critical strategies to help avoid lowball offers or denials on water damage claims:

Request the full claims file. Ask your insurer for a complete copy, including adjuster notes and communications. This can reveal missteps or missing documentation.

Watch for policy sublimits. Water damage claims may be subject to hidden sublimits — know the cap on your policy and whether it applies per occurrence or annually.

Submit proof of loss. Many policies require this formal document listing all damage and costs. Submitting one early can accelerate processing and protect your rights.

Track statutory deadlines. Many states have strict timelines for insurer response. Missed deadlines may entitle you to interest or penalties or support a bad-faith claim.

Hire a licensed contractor or engineer. Third-party documentation — especially for structural or mold-related damage — carries legal weight when disputing coverage decisions.

Real-World Example

In 2023, a Florida homeowner filed a $14,000 claim for water damage after a washing machine overflowed. The insurer initially offered $3,500. After consulting an attorney and providing detailed contractor estimates and a proof of loss, the homeowner settled for $13,200 — and the attorney’s filing of a Civil Remedy Notice for bad faith prompted a faster resolution.

Case Law Reference

In Branch v. Farmers Insurance Co., Inc., 55 P.3d 1023 (Okla. Civ. App. 2002), the court found the insurer liable for bad faith after it ignored contractors’ reports and undervalued water-damage repairs. The case reinforced that policyholders are entitled to fair consideration of all submitted evidence.

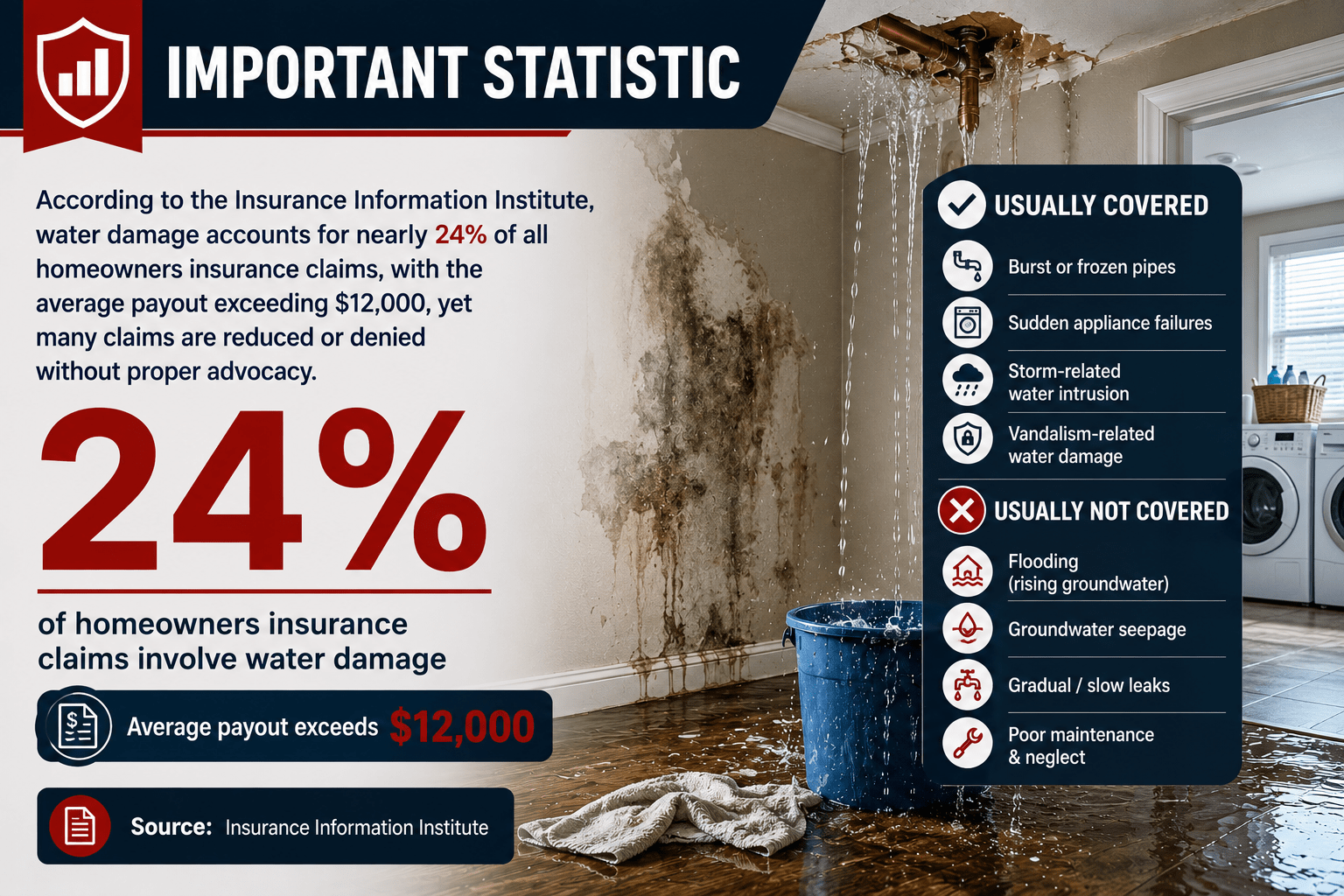

Important Statistic

According to the Insurance Information Institute, water damage accounts for nearly 24% of all homeowners insurance claims, with the average payout exceeding $12,000, yet many claims are reduced or denied without proper advocacy.

Summary

Understanding what your homeowners policy covers, what it excludes, and the additional coverages available makes a real difference. From sudden and accidental events to appliance failures and optional coverages like sewer backup and mold remediation, knowing your policy inside out is essential. By maintaining your property and preparing for seasonal changes, you can prevent water damage and reduce the likelihood of a claim. Equip yourself with the right information and take control of your coverage.

Frequently Asked Questions

Does homeowners’ insurance cover flood damage?

No, homeowners’ insurance does not cover flood damage. You’ll need a separate flood insurance policy for adequate protection.

Will my homeowners’ insurance cover water damage from a leaking roof?

Generally, yes, if the damage is sudden and accidental, such as from a storm. Damage resulting from poor maintenance, however, is typically not covered.

What should I do immediately after discovering water damage?

Identify and stop the source of the water to prevent further damage, document the damage with photographs, and notify your insurance agent to start the claims process.

Can I get coverage for sewer backup?

Yes, you can add optional sewer backup insurance to your homeowners policy to protect against damage from backed-up sewer lines.

How can I prevent water damage in my home?

Conduct regular maintenance of your plumbing, check for leaks, clean gutters, and prepare for seasonal changes. Proactive measures and routine inspections are essential to safeguarding your property.

Call or text (832) 323-3000 or complete a Free Case Evaluation form