Does homeowners’ insurance cover mold? Yes, but only if the mold is caused by a specific covered event, such as sudden water damage. Otherwise, mold damage is usually not covered. This article explains when mold is covered by insurance, potential exclusions, mold remediation coverage, and what to do if you find mold in your home.

Key Takeaways

✓

Homeowners’ insurance may cover mold damage caused by sudden and accidental water damage, but exclusions apply to neglect and maintenance issues.

✓

Preventing mold requires regular home maintenance, controlling humidity levels, and proper ventilation; homeowners should take proactive steps to avoid mold growth.

✓

If insurance coverage is lacking, alternative solutions include DIY cleanup for small infestations or hiring professional remediation services for extensive mold damage.

✓

Understanding mold remediation coverage in homeowners insurance policies is crucial. Policies often have limitations, and knowing what is covered can help homeowners manage potential costs and ensure they are adequately protected.

For a free legal consultation, call (832) 323-3000

Understanding Homeowners Insurance Coverage for Mold

Homeowners insurance protects against various risks, including financial losses from perils such as lightning, fire, hail, and vandalism. However, home insurance companies often find that mold coverage is more complex and requires a clear understanding of what is included and excluded in your policy.

Understanding your mold coverage involves reviewing your homeowners’ insurance policy and consulting with your insurance agent. This helps you identify any limitations or exclusions, allowing you to take preventive measures and consider additional coverage options. Mold remediation coverage often has specific limitations and may not cover all scenarios, so it’s crucial to understand the specifics of your policy to determine what is available.

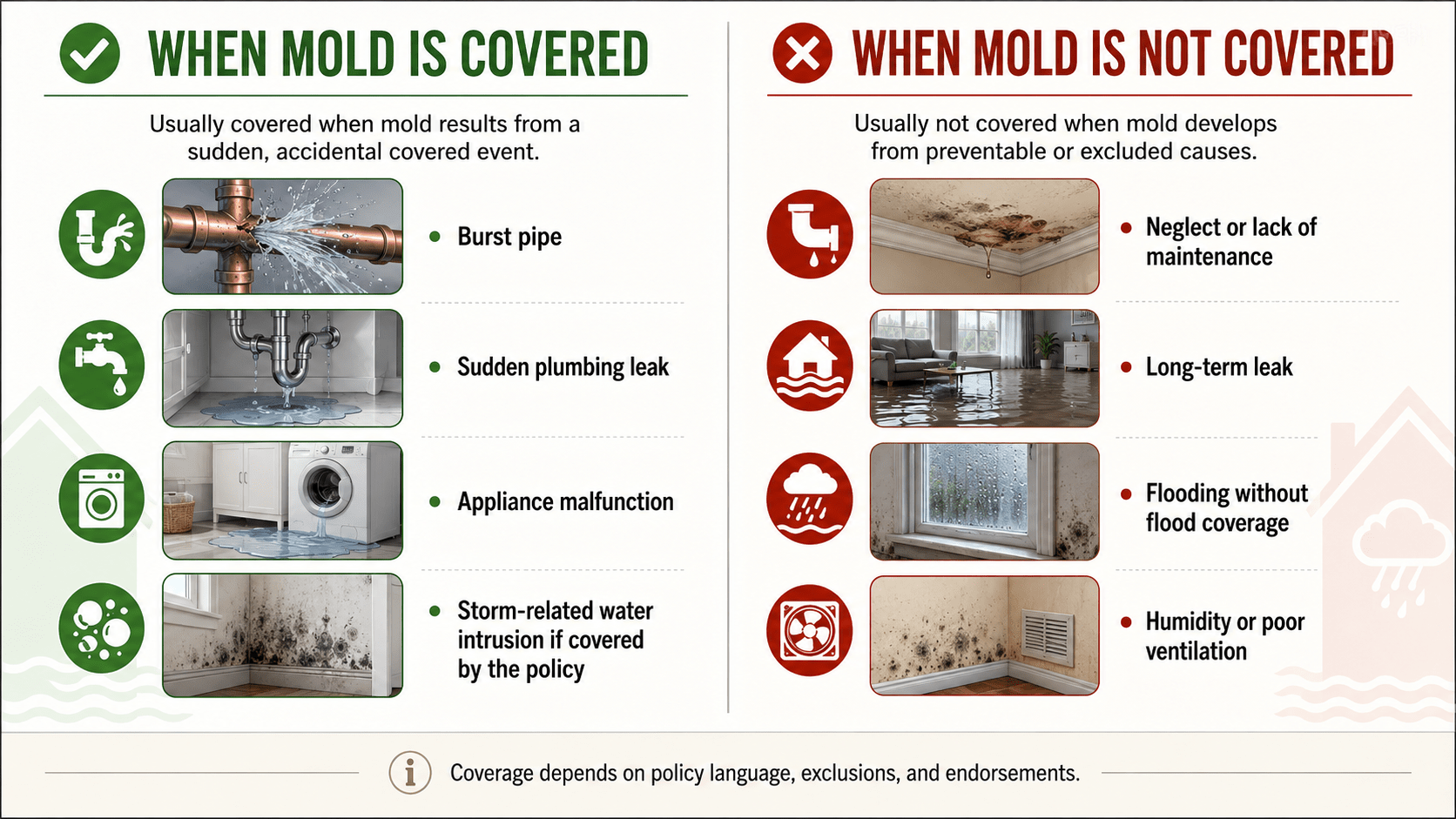

Mold damage might be covered by homeowners’ insurance if it results from a covered peril, such as sudden and accidental water damage. These conditions are typically specified within the policy. For instance, if a burst pipe or an appliance malfunction causes water damage that subsequently leads to mold, this scenario might be covered under your policy.

Understanding mold remediation coverage is crucial, as the costs involved can be significant. Knowing what your policy covers can help you prepare for these expenses.

However, mold coverage often includes limitations and specific conditions. Insurance companies may cover the costs of mold repair, removal, and testing, but these are usually subject to the policy’s terms and aggregate limits.

Sudden and Accidental Water Damage

Homeowners’ insurance may cover mold remediation if it results from sudden and accidental water damage. This includes incidents like sudden leaks or burst pipes, which are often unforeseen and require immediate attention. Common examples include leaks from washing machines, water heater failures, or burst pipes due to freezing temperatures or aging infrastructure. Mold remediation coverage typically applies in these scenarios, helping manage the costs of addressing mold damage.

Regular maintenance helps prevent such incidents. Proper drainage and prompt leak repair can protect your home from water damage that could lead to mold growth.

Acting swiftly to address water damage can mitigate further complications and potential mold infestations.

Covered Perils Leading to Mold

Homeowners insurance may also cover mold damage resulting from other perils explicitly listed in the policy. For example, if a storm causes a tree branch to break a window, resulting in water damage and subsequent mold growth, this scenario would typically be covered. Mold remediation coverage applies to mold resulting from these covered perils, ensuring that the costs of remediation are addressed by the policy.

In cases where mold issues arise from recent natural disasters, homeowners can explore state or federal disaster assistance programs for additional support.

Endorsements and Additional Coverage Options

Knowing the water and mold clauses in your homeowners’ insurance policy clarifies the extent of your coverage. Some policies offer limited mold coverage, but you can enhance this with a mold insurance endorsement, which increases coverage limits or types of expenses covered. A mold insurance endorsement can significantly improve mold remediation coverage by addressing the costs and scenarios typically excluded from standard policies.

Additional coverage options include endorsements for water backup coverage for sewers or drains, sump pump failure, and equipment breakdown, which can protect home systems and appliances that might contribute to mold growth. These options can provide more comprehensive protection against mold-related issues.

Many homeowners’ insurance policies exclude mold damage due to increased claims and vague language. Mold-exclusion situations often involve neglect, ongoing leaks, and flooding, all of which are preventable with regular maintenance and proper home care.

Common causes for denied mold claims include poorly sealed doors or windows, leaky faucets, and a lack of ventilation. Successful mold claims must demonstrate that the mold was not pre-existing and was not due to a lack of maintenance.

Expenses related to mold testing and remediation are often excluded, making it crucial for homeowners to understand these limitations. Understanding mold remediation coverage is essential to avoid unexpected expenses and ensure you know what your policy covers.

Neglect and Lack of Maintenance

Homeowners’ insurance does not cover mold damage caused by maintenance issues, underscoring the importance of regular upkeep. Common exclusions include long-term, unrepaired leaks and general negligence, such as a poorly maintained roof or failure to use a dehumidifier.

Ensuring consistent home maintenance can prevent such exclusions and protect your investment. Neglect can also affect mold remediation coverage, as insurance policies often exclude mold damage resulting from poor maintenance.

Flooding and Sewer Backup

Standard homeowners’ insurance policies do not cover mold resulting from flooding or sewer backup. Since flood damage is generally not a named peril, there are widespread exclusions for mold damage from such events.

To obtain mold coverage related to flood damage, homeowners must purchase separate flood insurance or an endorsement. An optional sewer backup endorsement can cover mold from sewer issues, providing additional protection. Mold remediation coverage is typically excluded in cases of flooding and sewer backup, making it crucial to review policy specifics to determine what coverage is available.

High Humidity and Poor Ventilation

High humidity and poor ventilation create ideal conditions for mold growth, posing significant risks for homeowners. Typically, homeowners’ insurance does not cover mold damage caused by long-term issues such as high humidity and poor ventilation.

Maintaining proper ventilation and controlling humidity levels are essential to prevent mold and avoid coverage exclusions. Additionally, understanding mold remediation coverage in your homeowners insurance policy is crucial, as it often excludes damage caused by mold.

State-Specific Considerations for Homeowners Insurance

Homeowners insurance policies can vary significantly from state to state, and it’s essential to understand the specific considerations for your state. Coverage limits, mandatory endorsements, and how mold exclusions are interpreted can vary by location, so review your policy and any state requirements that apply to mold coverage.

Filing a mold claim can be straightforward if you follow the correct steps. Homeowners insurance includes two types of mold claims: first-party claims for your property damage and third-party claims for liability if someone else is affected by mold exposure and incurs medical expenses. Notify your insurer immediately upon discovering extensive mold growth to initiate the claim process.

Filing a mold claim requires additional documentation to show preventive actions taken, similar to other insurance claims. File a claim as soon as possible after discovering the damage to avoid complications. If denied, you may need to cover the cleanup costs personally.

Immediate Actions to Take

Upon discovering mold, take immediate steps to prevent further damage and improve your claim’s chances of success. Demonstrate that the water damage was sudden, accidental, and promptly reported for potential coverage.

Quickly stop any leaks by shutting off the main water supply, and make temporary repairs to protect your home from further damage. Since mold can begin growing within 24 hours of water exposure, it is essential to act quickly to sanitize and dry affected areas.

Documenting Mold Damage

Accurate documentation is crucial for a successful mold damage claim. Take comprehensive photos and videos of the mold damage from various angles, and compile a detailed list of affected items. Document the mitigation and repair processes if mold appears after repairs.

This thorough documentation helps ensure your claim is processed smoothly and increases the likelihood of a favorable outcome, as insurance companies often require detailed evidence to determine the extent of coverage available.

Working with Your Insurance Agent

Consult your insurance agent to understand your mold coverage. Read your policy carefully or discuss it with your agent to know what is covered, including the specifics of your mold remediation coverage.

When hiring contractors for mold remediation, verify that they are licensed, insured, and experienced in handling mold issues. Your insurance agent can often recommend reputable contractors and provide guidance throughout the claims process.

Click to contact our property damage lawyers today

Preventing Mold in Your Home

Preventing mold in your home protects your health and property value. Mold damage is often preventable through proper maintenance, making regular home upkeep essential. Musty odors or slimy substances on surfaces can indicate mold growth, which can occur in areas such as linens, pillows, walls, bathrooms, and ceiling tiles due to moisture. Documenting all repairs and mitigation efforts is crucial to showing proactive maintenance.

Clutter can obstruct airflow, creating damp microclimates that encourage mold growth. Keeping your home tidy and ensuring proper ventilation can significantly reduce the risk of mold. Regularly checking for signs of mold and taking immediate action when you detect them can prevent extensive damage and health issues.

Regular Home Maintenance

Regular home maintenance is key to preventing mold growth. Consistently cleaning gutters ensures water is directed away from your home, preventing water from seeping into your foundation. Maintaining indoor humidity levels between 30% and 50% can mitigate mold growth, and promptly drying affected areas within 24–48 hours is crucial.

Proper ventilation in high-moisture areas like bathrooms and kitchens is essential. Insulating cold surfaces, such as pipes, can help prevent condensation, a significant contributor to mold issues. Regularly performing these tasks can help keep your home mold-free and protect your investment.

Controlling Moisture and Humidity

Controlling moisture and humidity is vital in preventing mold growth. Indoor humidity levels should ideally be maintained between 30% and 50% to inhibit mold. Using exhaust fans in kitchens and bathrooms can significantly reduce indoor humidity, while proper airflow and regular cleaning can further help prevent mold.

Routine inspections and repairs of roofs, plumbing, and windows are crucial for controlling moisture and preventing mold growth.

Using Proper Ventilation

Proper ventilation reduces moisture levels in your home, helping to prevent mold growth. Improving air circulation through ventilation reduces humidity, thereby mitigating the risk of mold. Using exhaust fans, especially in areas like bathrooms and kitchens, helps remove moisture from the air. Opening windows during dry conditions allows fresh air to circulate inside, lowering humidity.

Installing vents in attics and crawlspaces helps maintain proper airflow, significantly aiding in mold prevention. Regularly checking and maintaining ventilation systems can prevent moisture buildup that can lead to mold growth.

If your homeowners’ insurance does not cover mold damage, you are responsible for the cleanup. For small patches, a DIY approach might be sufficient, but extensive mold damage requires professional remediation services. If the mold is due to poor construction, seeking restitution from the responsible contractor might be an option.

Hiring professionals for mold remediation is essential, particularly for significant mold damage that poses health risks and structural concerns. Experienced professionals can ensure that the mold is properly identified and eliminated, reducing the risk of incomplete work and recurrence.

Exploring all available options can help manage mold issues effectively, even when insurance falls short.

DIY Mold Cleanup

For small mold infestations, DIY cleanup can be a practical solution. Wear protective equipment, including gloves, an N-95 respirator, and goggles when cleaning mold. Use a detergent-and-water mixture to clean mold from hard surfaces.

Ensure the affected area is thoroughly dried to prevent mold from returning. Regularly monitoring and maintaining your home’s cleanliness can keep minor mold issues under control.

Hiring Professional Mold Remediation Services

For extensive mold damage, hiring professional mold remediation services is highly recommended. Ensure the contractor you hire is licensed, insured, and experienced in mold remediation. Professionals can address health risks and structural concerns effectively, ensuring the mold is properly identified and eliminated. This reduces the likelihood of incomplete work and recurring issues, providing peace of mind and safeguarding your home.

Financial Assistance Programs

If mold damage is disaster-related, financial assistance from FEMA may be available through its Individuals and Households Program, which can help with cleanup and remediation. Various local programs also offer assistance to homeowners for health-related repairs, including mold remediation.

HUD provides information on state-specific resources for home repairs, including mold-related issues. The CDC funds programs aimed at preventing health hazards that may guide homeowners to mold-related assistance resources. Homeowners on tribal lands can access the Indian Home Loan Guarantee Program for rehabilitation, and the USDA offers loans and grants to very low-income homeowners for home repairs, including the removal of health hazards such as mold.

Legal Insight: Why Mold Coverage Matters

As one of the most contested areas in property damage insurance, mold claims often become battlegrounds between policyholders and carriers. Insurance companies may argue that mold is due to poor maintenance, while policyholders stress sudden accidental water damage. Having a skilled first-party insurance lawyer ensures your rights are protected and that exclusions are not unfairly applied to deny valid claims.

Real-World Example

For instance, after Hurricane Harvey in Texas, many homeowners discovered extensive mold damage from storm-related flooding. While standard homeowners’ insurance excluded flood damage, some policyholders with additional endorsements were able to recover significant remediation costs. This highlights the importance of understanding policy endorsements and state-specific laws.

Case Law Spotlight

A notable case is Fiess v. State Farm Lloyds, 202 S.W.3d 744 (Tex. 2006), where the Texas Supreme Court addressed whether mold damage caused by plumbing leaks was covered under homeowners’ insurance policies. The Court held that mold damage was excluded unless specifically covered by policy language, reinforcing the need to carefully review exclusions and endorsements.

Key Statistic

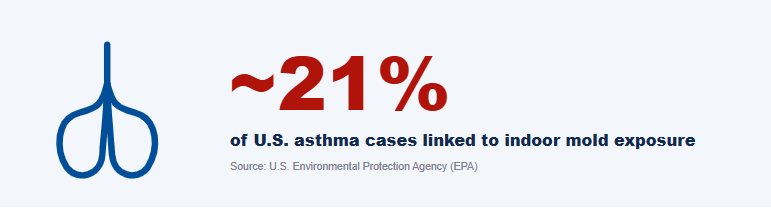

According to the Environmental Protection Agency (EPA), indoor mold exposure is linked to nearly 21% of asthma cases in the United States, underscoring both the health risks and the financial stakes involved in ensuring insurance coverage for mold remediation.

Attorney Tip

Always request a certified copy of your policy and review it annually. Even small wording changes in endorsements or exclusions can dramatically affect mold coverage. Consulting with a first-party insurance lawyer before a loss occurs can help you proactively identify and close coverage gaps.

Understanding when homeowners’ insurance covers mold damage can save you from unexpected financial burdens and ensure your home remains safe and healthy. By knowing the conditions under which mold is covered, the exclusions, and how to file a claim, you can navigate the complexities of mold insurance coverage effectively. Regular maintenance and preventive measures are crucial in managing mold risks. When insurance coverage falls short, alternative solutions like DIY cleanup, professional remediation, and financial assistance programs can provide the necessary support. Stay proactive and informed to protect your home from mold-related hazards.

Complete a Free Case Evaluation form now

Frequently Asked Questions

When does homeowners’ insurance cover mold damage?

Homeowners insurance covers mold damage when it results from a covered peril, such as sudden and accidental water damage from a burst pipe or an appliance malfunction. It’s essential to review your policy for specific coverage details.

What are some common exclusions for mold coverage under homeowners’ insurance?

Mold coverage under homeowners’ insurance typically excludes damage caused by neglect, lack of maintenance, high humidity, poor ventilation, and flooding or sewer backups unless specific endorsements are obtained. It’s essential to review your policy to understand these limitations.

How should I document mold damage for an insurance claim?

To effectively document mold damage for your insurance claim, take thorough photos and videos from multiple angles and create a list of all affected items. Also, ensure to include records of any mitigation or repair actions taken.

What steps can I take to prevent mold in my home?

To prevent mold in your home, maintain indoor humidity levels between 30% and 50%, ensure proper ventilation, address leaks promptly, and perform regular maintenance. These steps will significantly reduce the risk of mold growth.

What should I do if my homeowners’ insurance doesn’t cover mold damage?

If your homeowners’ insurance does not cover mold damage, handle small areas with a DIY cleanup, and for larger issues, hire professional remediation services. Additionally, explore financial assistance programs that may help cover the costs.

Call or text (832) 323-3000 or complete a Free Case Evaluation form