How an Appeal Letter Can Reverse a Denied Insurance Claim

A denied insurance claim can be frustrating, but an effective appeal letter can change the outcome. This article provides a sample letter of appeal for the reconsideration of insurance claims and offers tips on structuring your letter, what information to include, and how to present your case compellingly.

For a free legal consultation, call (832) 323-3000

For a free legal consultation, call (832) 323-3000

Key Takeaways

✓ An appeal letter is critical for contesting denied insurance claims and should include clear reasons for the appeal and thorough supporting documentation.

✓ Common reasons for claim denials include clerical errors, insufficient documentation, and missed deadlines, emphasizing the importance of accuracy and timely submissions.

✓ Persistence and professionalism in communication can significantly enhance the chances of a successful appeal, along with following proper submission protocols.

Understanding the Importance of an Appeal Letter

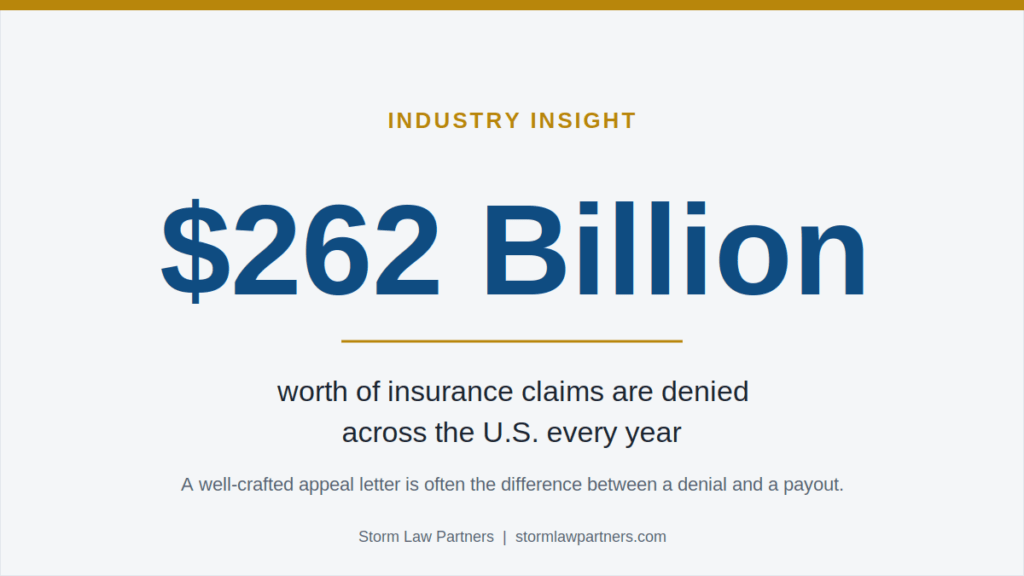

An appeal letter is essential for contesting denied insurance claims and seeking approval. Each year, $262 billion in insurance claims are denied, underscoring the need for effective appeals. A well-crafted appeal letter can enhance the chances of recovering denied claims. These letters formally request that the insurer reconsider its decision, allowing you to present additional information and clarify any misunderstandings.

Common scenarios that require an appeal letter include denied medical procedures and reimbursement claims. Minor errors in patient or claim information can lead to rejection, highlighting the need for accuracy. Omitting comprehensive evidence in the initial claim or appeal can limit the ability to consider the case, making thorough documentation vital.

The time frame for submitting an appeal for a denied long-term disability claim is typically 180 days, underscoring the urgency in the process. Knowing these timelines and the role of appeal letters enables you to act swiftly and effectively when your claim is denied.

Click to contact our property damage lawyers today

Common Reasons for Insurance Claim Denials

Insurance claim denials can occur for a variety of reasons. A common issue is a misunderstanding or oversight during the review process. For instance, clerical errors or misinterpretations of policy terms can lead to a denial despite the claimant being entitled to the benefits.

Another frequent reason is insufficient documentation, which is necessary to prove that the treatment was medically necessary. Missed submission deadlines are also a significant factor. Insurance companies have strict timelines for filing claims and appeals, and missing these deadlines can result in automatic denial.

Additionally, issues with out-of-network providers can lead to denials, as health insurers often have specific networks of approved providers and may not cover services from those outside the network.

Recognizing these common reasons helps in better preparing your initial claim and appeal. Including all necessary documentation, meeting deadlines, and ensuring services fall within the network can reduce the risk of denial and improve your appeal’s success.

Complete a Free Case Evaluation form now

How to Write an Effective Appeal Letter

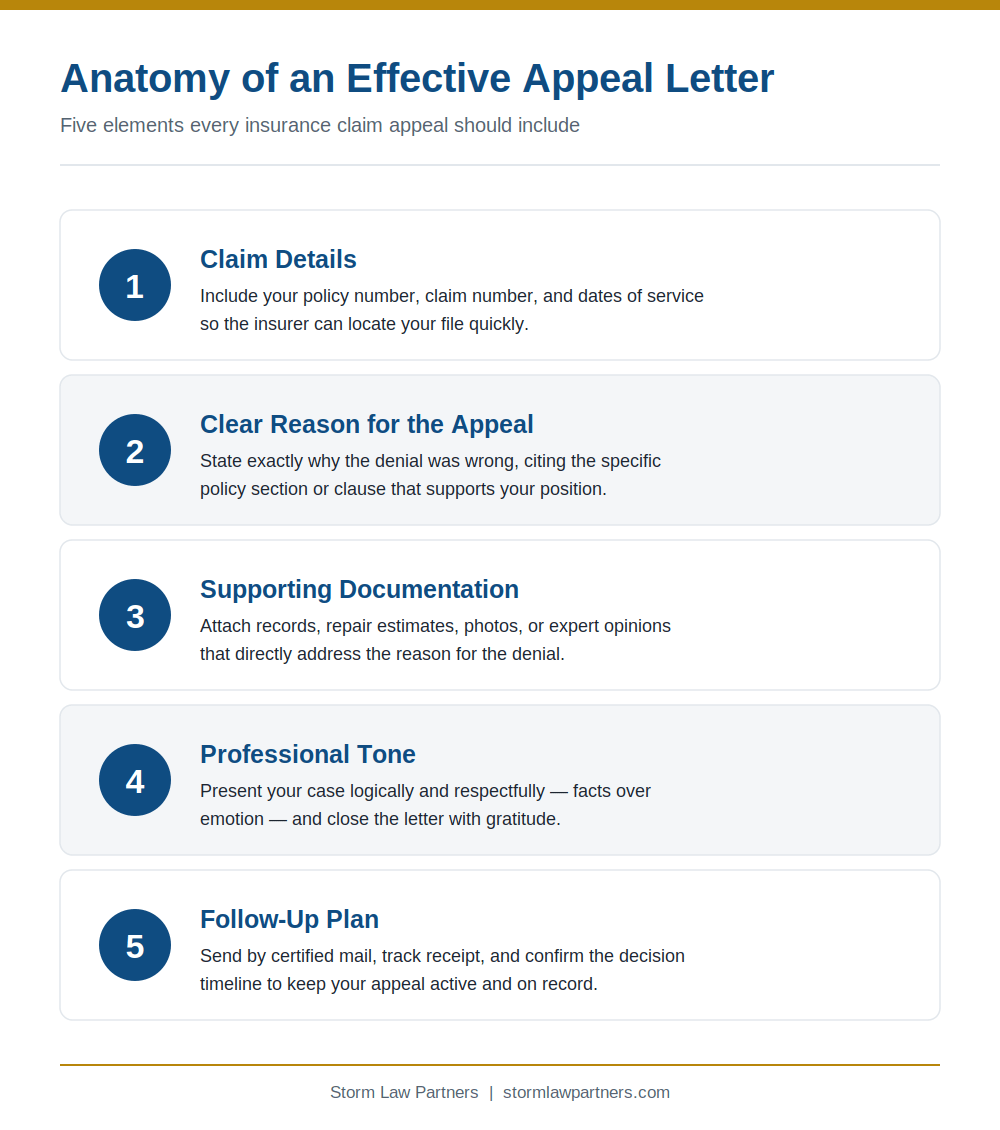

An effective appeal letter involves several key components. Begin by clearly outlining the reason for the appeal, such as a lack of coverage or a misunderstanding of policy terms. The letter should include specific claim details, such as policy numbers and dates of service, to ensure the insurer can easily locate your claim.

Supporting documentation is crucial as it strengthens your argument. This might include medical records, expert opinions, or additional evidence that addresses the reasons cited in the denial letter. Clarifications should directly address these reasons to make your case as strong as possible.

Professionalism in tone is essential. Focus on presenting your case logically and respectfully, avoiding emotional language. Concluding the letter sincerely with gratitude can enhance the overall tone and professionalism of the communication.

Following up after submitting an appeal demonstrates commitment and keeps your case active. A well-organized and professionally written appeal letter can significantly ease the review process for the insurance company and enhance your chances of a successful appeal.

Sample Appeal Letter for Incomplete Information Claims

A well-structured appeal letter for incomplete information claims typically includes an introduction stating the purpose, a body explaining the reasons for the appeal, and a conclusion urging a favorable response. Summarize the missing information and provide detailed explanations, along with supporting documents, to strengthen your appeal.

A brief explanation for any previous insufficiencies in the initial submission can help clarify issues raised in the denial letter. Supporting documents, such as medical records or expert opinions, can further substantiate your case. Expressing hope for a prompt review and favorable reconsideration can positively influence the outcome.

Sample structure for your appeal letter:

- Introduction: State the letter’s purpose.

- Body: Detail the reasons for the appeal, summarize missing information, and include explanations.

- Conclusion: Urge a favorable reconsideration and express gratitude for the review.

Sample Appeal Letter for Lack of Coverage Claims

When appealing a lack-of-coverage claim, the letter should clearly state this as the reason for the denial. Start by explaining the medical necessity of the treatment and how it aligns with the policy terms. Provide detailed explanations and any supporting evidence that demonstrates why the treatment should be covered. This approach ensures the insurer understands the importance of the treatment and the justification for coverage.

Sample structure:

- Introduction: State the claim number and the reason for the denial.

- Body: Explain the medical necessity, provide test results, and include any relevant documentation.

- Conclusion: Request reconsideration and express hope for a favorable outcome.

Sample Appeal Letter for Insufficient Documentation Claims

For claims of insufficient documentation, your appeal letter should describe the member’s medical condition and the consequences of not receiving treatment. Refer to the medical-necessity justification and support from the treatment team to strengthen your case.

Specify the missing documents and briefly describe the information originally submitted. Include supporting documents to substantiate the additional information provided in the appeal. State clearly the need to reconsider the claim due to insufficient documentation.

Sample structure:

- Introduction: State the claim number and reason for denial.

- Body: Describe the health condition, justify medical necessity, and outline missing documents.

- Conclusion: Request reconsideration and express gratitude.

Sample Appeal Letter for Missed Deadline Claims

For missed-deadline claims, your appeal letter should include a subject line such as “Appeal for Reconsideration of Claim [Claim Number] Due to Missed Deadlines.” Explain the circumstances that led to the missed deadline and request reconsideration, providing relevant details.

In these situations, persistence and professionalism are crucial. Maintain a respectful tone throughout the letter, and ensure that all relevant information is clearly presented. This increases the chances of a successful reconsideration despite the missed deadline.

Tips for Submitting Your Appeal Letter

When submitting your appeal letter, ensure it is sent via certified mail with return receipt requested, or through fax, email, or hand delivery for expedited review. Timely follow-ups after a claim denial ensure that appeal deadlines are met.

Inquire about the expected timeline for a decision when following up on your appeal. Tracking the appeal process ensures it is received and processed correctly. These steps can help ensure that your appeal is given the prompt attention it deserves.

The Role of External Reviews in Appeals

Independent organizations conduct external reviews to ensure unbiased evaluations of denied claims. They can be sought for both medical and coverage denials, offering a comprehensive evaluation of the claim. Consumers can initiate an external review within four months of receiving a claim denial notice.

Insurance companies must accept the findings of the external review and act promptly. The process is usually initiated without additional cost to the insured individual, making it a valuable resource in the appeal process.

Staying Persistent and Professional

Persistence can significantly influence insurance companies to reconsider denied claims. Persistence and thoroughness are crucial when navigating the insurance claim appeal process. A calm and respectful tone in your appeal letter can positively influence the review process.

Keep detailed records of all communications with the insurance company regarding your appeal. Regularly check in via phone or email to ensure progress. This level of diligence and professionalism can improve the likelihood of a favorable outcome in the appeal process.

Attorney Insights: How to Make Your Insurance Appeal Letter Legally Strong

As a first-party insurance attorney, I’ve seen hundreds of appeals succeed—and fail. To give your appeal the best shot at success, consider these advanced legal tips:

- Reference Your Policy Language: Quote the exact section or clause in your policy that supports your position. This shows legal merit and reduces interpretation errors.

- Attach a Sworn Statement: A notarized declaration of facts can add legal weight and help in cases that escalate to litigation.

- Include a Timeline of Events: A clear chronology helps reviewers understand delays, miscommunications, or procedural missteps by the insurer.

- Use Legal Terminology Carefully: Phrases such as “good faith,” “material evidence,” and “duty to indemnify” convey seriousness and professionalism.

- Request a Claims File Copy: You have the right to request the insurer’s file for your case, which may include critical notes that justify denial or delay.

Summary

A denied insurance claim is rarely the final word. A clear, well-documented appeal letter gives you the chance to correct errors, supply missing evidence, and ask the insurer to reconsider. The strongest letters state the specific reason for the appeal, include your claim details, attach supporting documentation, and maintain a professional, respectful tone from start to finish.

Just as important as what you write is how you follow through. Send your appeal through a trackable method, meet every deadline, and keep records of all communication. If the insurer upholds the denial, an independent external review—available within four months of the denial notice and usually at no cost—offers another path. Persistence, organization, and professionalism consistently improve your odds of turning a denial into an approval.

Frequently Asked Questions

What is an insurance claim appeal letter?

An insurance claim appeal letter is a formal written request asking your insurer to reconsider a denied claim. It lets you present additional information, clarify misunderstandings, and explain why the claim should be approved under your policy terms.

What are the most common reasons insurance claims get denied?

The most common reasons include clerical errors or misinterpreted policy terms, insufficient documentation, missed filing deadlines, and issues with out-of-network providers. Many denials come down to oversights that a well-supported appeal can address.

What should an effective appeal letter include?

An effective appeal letter should include your claim details (such as policy and claim numbers and relevant dates), a clear reason for the appeal, supporting documentation that addresses the denial, and a professional, respectful tone. Following up after submission helps keep your case active.

How long do I have to appeal a denied insurance claim?

Deadlines vary by policy and claim type—for example, appeals for denied long-term disability claims are often due within 180 days. Always check your denial letter for the specific deadline, and act promptly to avoid forfeiting your right to appeal.

What is an external review, and when can I request one?

An external review is an impartial evaluation of your denied claim conducted by an independent organization. You can generally request one within four months of receiving a denial notice, usually at no additional cost, and the insurer must accept and act on the findings.

Call or text (832) 323-3000 or complete a Free Case Evaluation form