When your roof is damaged, knowing how to negotiate a roof replacement with your insurance company is crucial. You’ll need to understand your policy, thoroughly document all damage, and present a compelling case to your insurer. This guide provides actionable steps to help you navigate the claims process and maximize your insurance coverage.

For a free legal consultation, call (832) 323-3000

Key Takeaways

✓ Thoroughly review your homeowners’ insurance policy to understand coverage types such as Actual Cash Value (ACV) and Replacement Cost Value (RCV), as they dictate the financial outcome in roof replacement claims.

✓ Document all roof damage comprehensively with photographs and detailed notes to strengthen your insurance claim, and consider hiring a reputable roofing contractor for an accurate assessment.

✓ Preparation and persistence in negotiations with your insurance company are critical; gather multiple contractor estimates and supporting evidence to ensure a fair settlement.

For a free legal consultation, call (832) 323-3000

Review Your Homeowners Insurance Policy

Thoroughly reviewing your homeowners’ insurance policy is an essential first step in the claims process. This helps you understand what your insurance covers and any applicable deductibles. Coverage can vary significantly depending on your roof’s age and the nature of the damage. Common exclusions include neglect, regular wear and tear, and specific events such as floods, which could result in denied coverage.

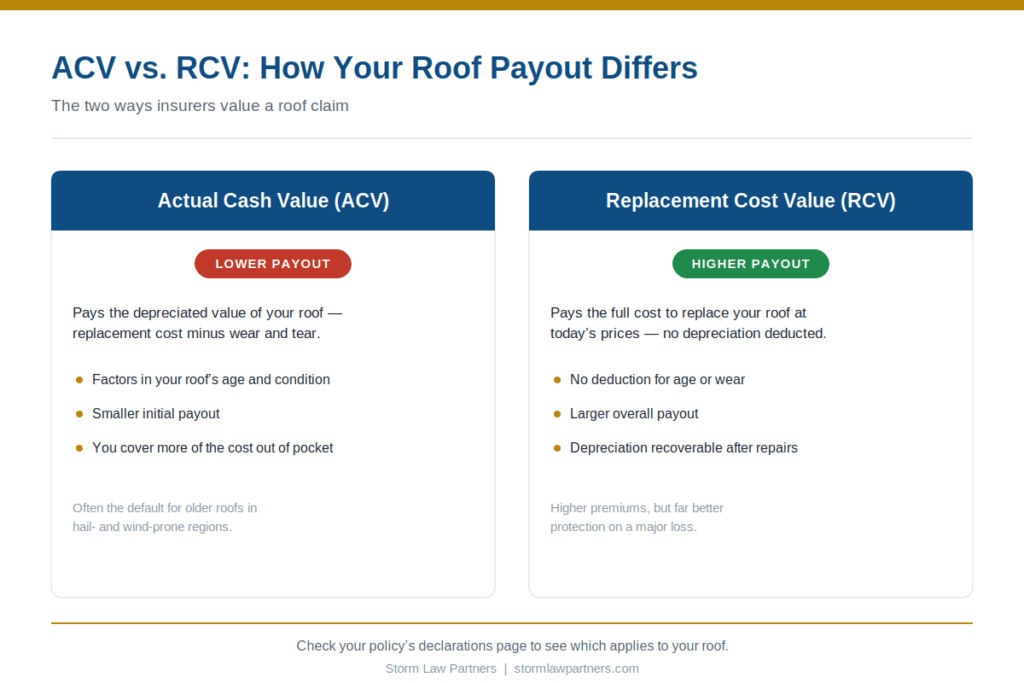

Many homeowners mistakenly believe their policy covers 100% of all roof damage, which is often not the case. Grasping the distinctions between Actual Cash Value (ACV) and Replacement Cost Value (RCV) policies will guide your approach. ACV provides the depreciated value of your roof, while RCV covers the full replacement cost minus the deductible. This distinction plays a crucial role in how you approach your roof replacement claim.

Actual Cash Value (ACV) Coverage

An Actual Cash Value (ACV) policy calculates the payout based on the depreciated value of your roof, taking into account both depreciation and current market value. This means that if your roof is older, the payout might be significantly lower—potentially covering as little as 15% of the replacement cost. If the payout from an ACV policy is insufficient for a full roof replacement, you will need to cover the difference out of pocket.

Recognizing the limitations of an ACV policy is important. If your roof is older and the payout is minimal, you might face substantial out-of-pocket expenses. Knowing the specifics of your policy helps you make informed decisions when negotiating with your insurance company.

Replacement Cost Value (RCV) Coverage

Replacement Cost Value (RCV) policies cover the cost of replacing your roof, ensuring it returns to a brand-new condition. RCV policies pay the replacement cost minus the deductible, covering the full cost without depreciation. However, for any upgrades or enhanced materials, you will be responsible for paying the difference.

An RCV policy is beneficial because it restores your roof to its most recent condition. This type of coverage is particularly advantageous if you want to avoid the financial burden of non-recoverable depreciation. Identifying whether your policy is RCV or ACV will greatly influence your claim strategy.

Assess and Document Roof Damage

Thoroughly assessing and documenting roof damage is vital for supporting your insurance claim and avoiding complications. Start with an initial inspection to identify visible damage, such as missing shingles or granule loss. Documenting significant damage promptly can make a substantial difference in the outcome of your claim. Detailed photographs and notes will serve as evidence and will be invaluable when presenting your case to the insurance company.

Initial Inspection

During the initial inspection, look for visible issues like missing shingles, cracks, holes, and loose materials. Check gutters, downspouts, and flashing around chimneys and vents for signs of water damage. Document any signs of collateral damage found on the ground around the house.

Being thorough during this inspection is important. Missing, cracked, or curled shingles and damaged flashing are red flags that need attention. Routine maintenance and timely inspections can help you spot these issues early, preventing more significant problems in the future.

Detailed Documentation

When documenting roof damage, include detailed photos and videos from multiple angles with time and date stamps. This comprehensive documentation will support your insurance claim and expedite processing.

Alongside photographic evidence, maintain detailed notes and records of prior maintenance and roof conditions. These records can strengthen your case and demonstrate that the roof was in good condition before the damage occurred.

Click to contact our property damage lawyers today

Hire a Reputable Roofing Contractor

Engaging a reputable roofing contractor is a critical component in the roof replacement process. Homeowners can choose their own roofing contractor regardless of insurance company recommendations. A reliable contractor will assess the damage, document the condition with photos, and provide a written evaluation.

Having a detailed roofer’s report on the roof’s condition can significantly aid discussions with your insurance company, providing a professional assessment that adds credibility to your claim.

Choosing the Right Contractor

Locating a roofer experienced with insurance claims is crucial. Confirm that your contractor is licensed and insured to prevent complications during the roof replacement process. Obtaining three or four detailed estimates from roofing professionals can provide a range of options and help in negotiations.

Written estimates from roofing contractors should include costs, materials, and labor for clarity during negotiations. This ensures transparency and helps you understand what exactly is covered.

Contractor’s Report

A contractor’s detailed report helps clarify the scope of damage and necessary repairs for insurance claims. Detailed reports and expert opinions can bolster the credibility of your claim and support your settlement request.

Including a variety of documentation types, like contractor assessments and weather reports, can strengthen the argument for a roof replacement claim. This comprehensive approach ensures all aspects of the damage and necessary repairs are thoroughly documented.

Complete a Free Case Evaluation form now

Contact Your Insurance Company

Once you’ve assessed the damage and gathered documentation, contact your insurance company to start the claims process. Reach out as soon as you notice roof damage and request that an adjuster come to assess it. The adjuster will inspect the roof and determine coverage for the repairs. Having a reputable roofing contractor already involved can offer guidance during the process and help ensure a better outcome.

Filing the Claim

Provide thorough documentation when filing your roof damage claim to support your case. Photographic evidence of the damage, along with a detailed report from a roofing contractor, is essential for a robust claim. The timeframe to file your roof damage claim is typically between 30 and 60 days from the date of damage, though you should always check your policy.

Consulting roofing contractors before submitting the claim can offer invaluable support and insights. Their expertise can help you understand the extent of the damage and the necessary repairs.

Meeting with the Adjuster

An insurance adjuster will be assigned to assess the damage after you report it. Being present during the adjuster’s assessment allows you to highlight all observed damage and discuss your contractor’s findings.

Discussing your contractor’s findings helps ensure all damage is considered during the adjuster’s assessment. Confirm that your contractor provides a detailed invoice that separately lists the costs covered by insurance and any additional expenses.

Click to contact our property damage lawyers today

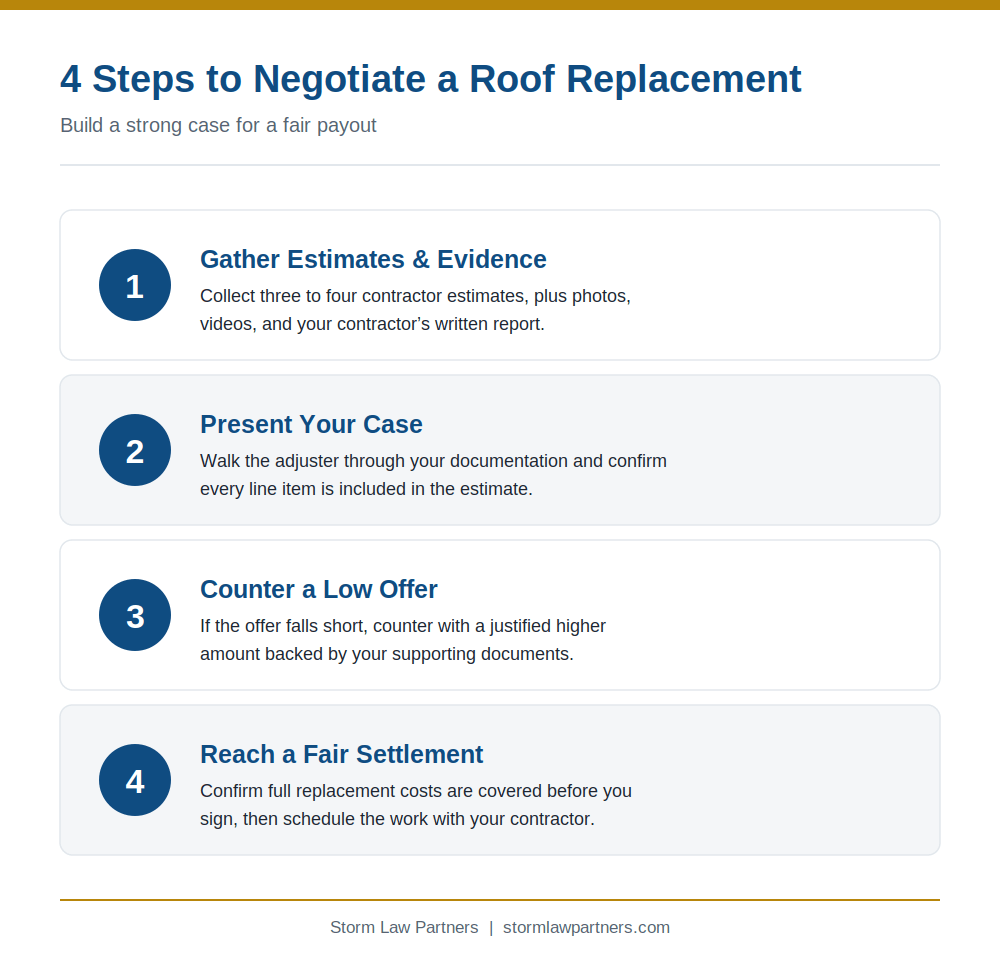

Prepare for Negotiation

Preparation is key when negotiating a roof replacement. Gather all necessary information and documentation before negotiating with your insurance company. Homeowners should expect a fair payout for roof damage in return for paying substantial premiums. Visual evidence and multiple estimates can significantly improve your chances of a complete settlement.

Collect Multiple Estimates

Securing multiple quotes from contractors helps determine replacement costs and strengthens your negotiation position. Getting multiple estimates helps you assess the cost accurately and provides relevant information to the insurance adjuster; seeking a second opinion can further enhance your understanding of the costs involved. For a benchmark, see the typical average insurance payout for hail damage to a roof.

Securing multiple quotes from contractors can reveal pricing discrepancies and help you justify your claim to the insurance company. This thorough approach will strengthen your case during negotiations.

Build Your Case

Evidence that the entire roof was in great condition before the storm damage is beneficial when filing a roof replacement claim. Gather comprehensive photos and videos of your roof damage to support your claim. Estimates from various contractors validate the need for a full roof replacement during discussions with your insurer.

An insurance estimate for roof replacement should include local codes, labor, dump fees, overhead, profit, and other necessary line items. When requesting a higher payout, justify your request with details on the extent of the damage and the costs of materials and labor.

Negotiate with Your Insurance Company

Negotiating with your insurance company requires preparation, documentation, and persistence. Persistence and politeness throughout the process can enhance your chances of success. A strategic negotiation approach can greatly increase your chances of receiving a fair settlement. If the initial offer is insufficient, negotiate by providing additional evidence or quotes to strengthen your request.

Presenting Your Evidence

RCV policies should cover everything a roofer needs to do the job correctly. An ITEL report, which analyzes a shingle sample, can identify the brand and specific color of the asphalt shingles. Ensure that all necessary line items are included in the insurance estimate for roof replacement. Presenting this evidence effectively can make a significant difference in the negotiation.

Countering Offers

Compile all documentation related to damage assessments and repair estimates to strengthen your counteroffer. You may need to provide detailed justification for a higher payout based on the damage assessment and material costs. If the initial offer is insufficient, counter with a justified higher amount and submit supporting documents for the insurance company’s review.

Hiring a Public Adjuster

Public adjusters can help identify overlooked damages in the claims process, which may lead to a more favorable outcome. A public adjuster typically operates on a contingency fee basis, meaning they take a percentage of the settlement. Engaging a public adjuster can improve your chances of a fair settlement, helping you navigate the claims process and ensure all damages are accounted for.

Finalizing the Settlement and Repairs

After agreeing on the settlement, schedule the roof replacement with your contractor and ensure compliance with local building codes. The insurance company will determine the amount paid for either a partial repair or a total roof replacement.

Reviewing the Settlement Offer

Confirm the settlement includes full replacement costs, as missed items can lead to inadequate coverage. Under RCV coverage, homeowners receive a reimbursement check after completing the roof replacement, covering most of the remaining expenses. Pay the deductible before work begins. If the settlement offer falls short, take action to pursue the complete cost of roof replacement, and review the offer thoroughly to avoid surprise expenses later.

Scheduling the Work

Schedule roof repairs with your contractor promptly to prevent further damage and protect your home. Ensure your contractor invoices for the covered portion of the roof replacement costs. All work should comply with local building codes and industry standards—this is not only a legal requirement but also ensures the longevity and durability of your new roof.

Legal Rights and Insurance Obligations

Understanding your legal rights during the insurance negotiation process is paramount. Policyholders are entitled to fair treatment under the Unfair Claims Settlement Practices Act (UCSPA), which requires insurers not to unreasonably delay, deny, or underpay valid claims. This knowledge can empower you to push back if your insurer acts in bad faith—and to understand your options for suing an insurance company for denying a claim.

Case Law Reference

In Windridge of Naperville Condominium Ass’n v. Philadelphia Indemnity Insurance Co., 932 F.3d 1035 (7th Cir. 2019), the court addressed a policyholder’s right to full replacement cost after storm damage, reinforcing the importance of policy language and comprehensive documentation. This case illustrates how legal precedent can support your negotiation efforts.

Real-World Example: Success After a Denied Claim

After a Texas hailstorm in 2023, a homeowner initially received a denial for roof replacement due to “insufficient damage.” By hiring a licensed contractor and a public adjuster, they re-documented the damage and filed an appeal. Within 60 days, the insurer reversed its decision and issued a full payout under the homeowner’s RCV policy. This underscores how persistence and professional support can lead to successful outcomes.

Crucial Statistic to Know

Industry data from the National Association of Insurance Commissioners (NAIC) indicates that a large share of disputed homeowners’ insurance claims result in higher payouts after an appeal or legal action. This emphasizes the value of not accepting the first offer and using every resource—contractors, documentation, and legal knowledge—to negotiate effectively.

Summary

Navigating the roof replacement claim process with your insurance company can be challenging, but with the right knowledge and preparation, it’s manageable. Reviewing your homeowners insurance policy, assessing and documenting roof damage, hiring a reputable roofing contractor, and effectively negotiating with your insurer are the crucial steps.

By following these proven tips, you can pursue a fair settlement and a smooth roof replacement process. Persistence and thorough documentation are key to a successful claim. Take control of the process and secure the best outcome for your home.

Frequently Asked Questions

What should I do first when I notice roof damage?

Quickly assess and document the roof damage, then reach out to your insurance company to initiate the claims process.

How do I know if my policy is ACV or RCV?

Review your homeowners insurance policy or consult your insurance agent to determine whether your coverage is Actual Cash Value (ACV) or Replacement Cost Value (RCV).

Why is it important to hire a reputable roofing contractor?

A reputable roofing contractor ensures quality workmanship and provides detailed documentation, which is essential for a successful insurance claim. This protects your investment and helps ensure the project meets industry standards.

What if the insurance company’s initial offer is insufficient?

Gather additional evidence, obtain multiple estimates, and negotiate for a higher settlement. Hiring a public adjuster can also help advocate for your claim.

How long do I have to file a roof damage claim?

You generally have between 30 and 60 days from the date of damage to file a roof damage claim, but always review your specific policy for any unique requirements or deadlines.

Call or text (832) 323-3000 or complete a Free Case Evaluation form

Call or text (832) 323-3000 or complete a Free Case Evaluation form