Wondering how much you could get from your insurance if your home suffers water damage? The average insurance payout for water damage claims is around $11,605. This amount gives you an idea of the financial support you can expect from your insurer. In this article, we’ll break down what influences these payouts, typical costs, and more to help you better understand water damage claims.

Key Takeaways

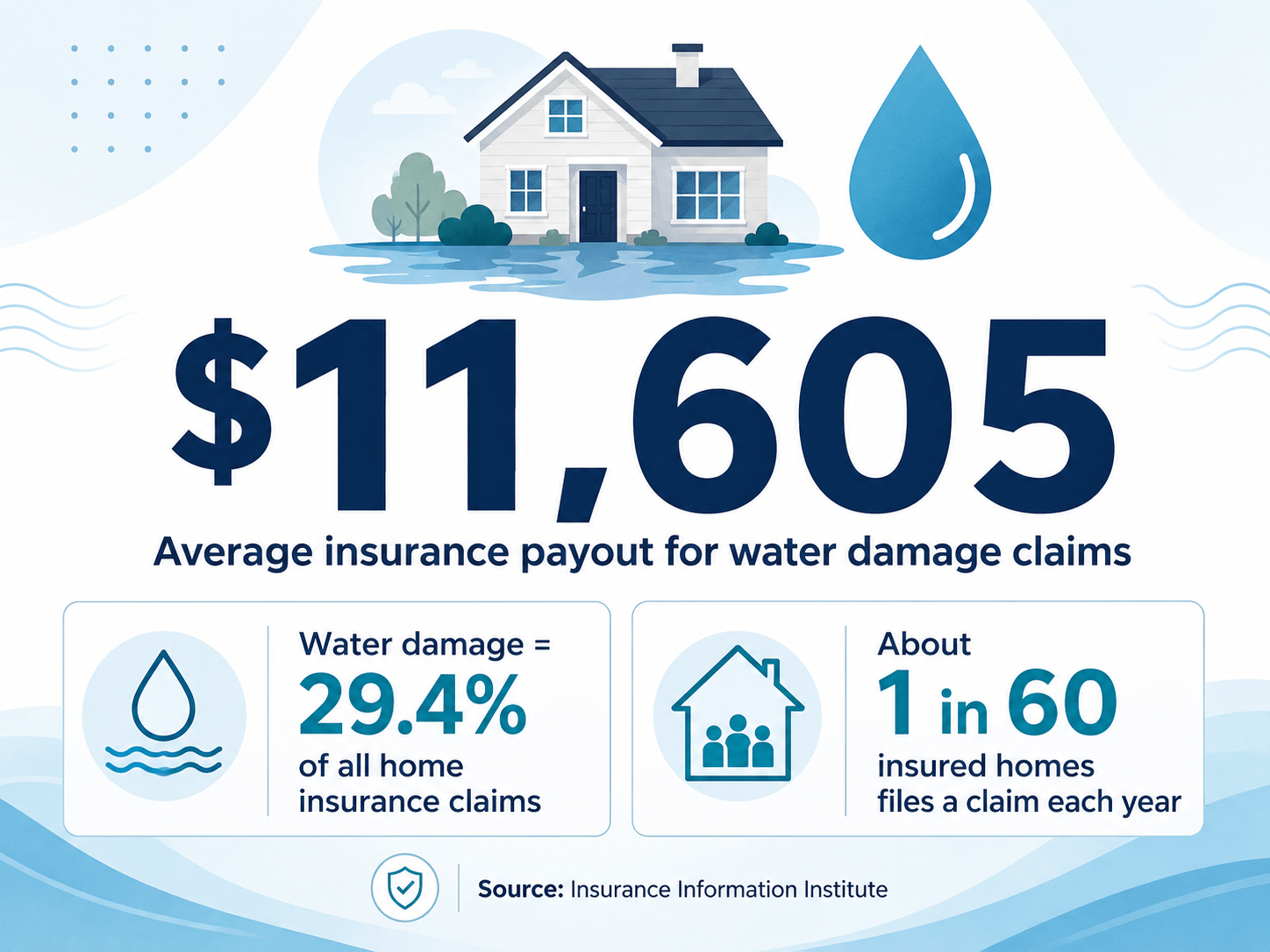

The average insurance payout for water damage claims is approximately $11,605, with water damage accounting for 29.4% of all home insurance claims.

Factors influencing payout amounts include the extent of damage, type of water contamination, and location, with extensive damage leading to significantly higher restoration costs.

Homeowners insurance typically covers unexpected water damage from events like burst pipes but does not cover flood damage, emphasizing the need for additional flood insurance in at-risk areas.

The average insurance payout for water damage claims is approximately $11,605, reflecting the substantial financial burden these incidents can impose on homeowners. With water damage accounting for 29.4% of all home insurance claims, it’s clear that this is a prevalent issue.

Annually, about 1 in 60 insured homes file claims for water damage or freezing damage, underscoring the frequency of these events. Typical claim amounts vary, but they often average around $7,000, underscoring the need for homeowners to understand potential costs and prepare accordingly.

Understanding average insurance payouts helps homeowners grasp the severity and financial implications of water damage.

1. Factors Influencing Payout Amounts

Several factors can significantly influence the payout amount for water damage claims. The extent of the damage, the type of water contamination, and the location of the damage all play crucial roles in determining the final payout. More extensive damage typically results in higher payouts due to increased restoration costs.

The type of water contamination — whether it’s clean, grey, or black water — also affects restoration costs and, consequently, insurance payouts. Additionally, the location of the leak can affect repair costs due to varying labor and material prices in different areas.

Variations in insurance policy coverage and extent can directly influence payout amounts. Higher deductibles in insurance policies lead to lower payouts, making it crucial to understand your policy’s terms.

Legal Insight

From a legal standpoint, homeowners should also consider how their prompt response to damage and communication with the insurer can impact their claim. Maintaining a comprehensive inventory of home contents, securing a certified restoration estimate, and consulting a public adjuster when necessary can significantly increase the likelihood of a favorable payout. Legal representation early in the claims process may help counteract lowball settlement offers and ensure full policy entitlements are respected.

2. Typical Range of Payouts

The typical range of insurance payouts for water damage claims can vary significantly, illustrating the importance of accurately assessing the damage. On average, the cost of restoring water damage is $3,822, with a typical range of $1,361 to $6,282. Minor claims typically result in smaller payouts; extensive damage often leads to larger settlements.

This variability underscores the need for thorough documentation and assessment to secure a fair payout, as outcomes may vary depending on the circumstances.

Real-World Example

In 2021, a Houston homeowner received a $45,000 payout after a burst pipe during a winter storm caused extensive damage. The homeowner had thoroughly documented the damage and engaged a water damage specialist early on, which helped substantiate the claim and increase the settlement offer.

For a free legal consultation, call (832) 323-3000

Cost Breakdown of Water Damage Restoration

Restoring water damage can be a costly endeavor, with expenses varying widely based on the severity and type of damage. Restoration costs typically range from $1,322 to $5,954, depending on the extent of the damage and the materials affected. Minor water damage can be relatively inexpensive to repair, ranging from $150 to $400, while severe damage may cost between $20,000 and $100,000.

Knowing these expenses helps homeowners prepare for financial impacts and ensure adequate insurance coverage.

Classes of Water Damage

Water damage is categorized into four distinct classes, each reflecting the severity of the damage and the evaporation rate. Class 1 damage involves minimal water presence, often limited to a small area with low absorption.

In contrast, Class 4 damage includes extensive saturation, affecting low-porosity materials such as hardwood and brick, and requiring specialized drying techniques. These classifications significantly influence restoration costs and techniques.

Area-Specific Costs

The location of the water damage can greatly influence the restoration costs. For instance, wall leaks often lead to higher costs due to potential mold growth and the need for extensive repairs. Restoration costs for water-damaged plumbing typically range from $1,000 to $4,000, while costs for blackwater damage are approximately $7 to $7.50 per square foot. Costs vary significantly based on damage class, with Class 4 potentially reaching hundreds of thousands of dollars.

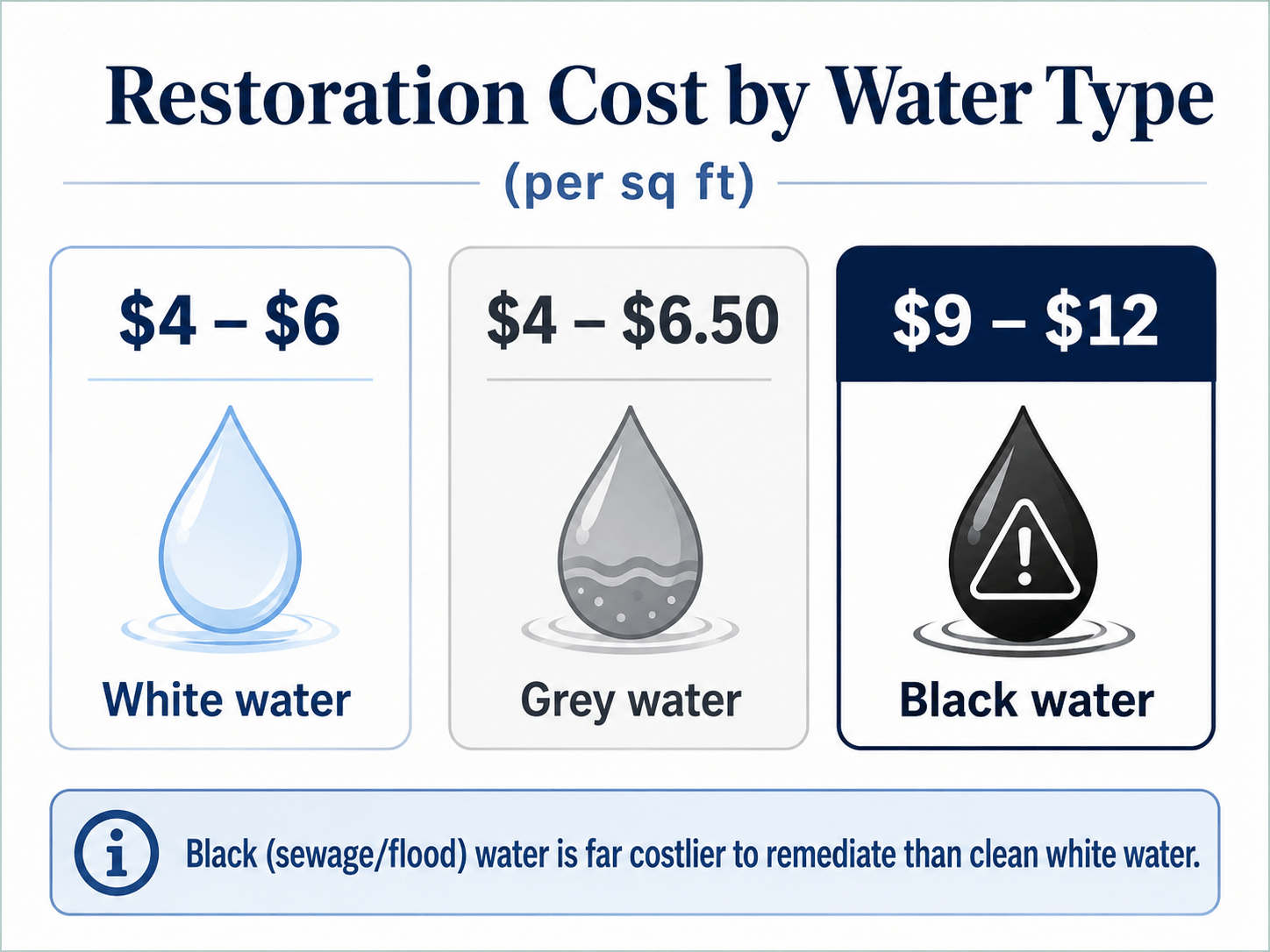

The level of water contamination plays a crucial role in determining the restoration costs. Clean water, or white water, is the least expensive to restore, whereas grey water and black water require more extensive and costly cleanup due to their higher levels of contamination.

Each water contamination category presents unique challenges and costs, highlighting the need for prompt action to mitigate financial impacts.

White Water

White water, the cleanest type of water damage, typically has lower restoration costs than contaminated water. Restoration involving clean water typically ranges from $4 to $6 per square foot. Since white water poses lower health risks, the cleanup process is less extensive, making it more affordable.

Timely action is essential, even in whitewater, to prevent escalation to more severe damage.

Grey Water

Grey water damage requires more extensive cleaning and treatment, leading to higher restoration costs than white water. Costs for restoring greywater damage range from $4 to $6.50 per square foot, reflecting the additional effort required to address contamination.

Greywater originates from sources such as sinks, showers, and washing machines, and while it contains lower levels of contamination than blackwater, it still requires careful handling and treatment to prevent health risks.

Black Water

Blackwater damage is the most expensive to restore due to its hazardous nature and often results from sewage issues or severe flooding. Restoration costs for blackwater can range from $9 to $12 per square foot due to the extensive cleanup required to ensure safety. Blackwater poses significant health risks from harmful pathogens and sewage, making thorough, specialized cleanup essential.

Water damage can result from various sources, each with its own set of associated costs. Common causes include severe weather events, leaky pipes and appliances, and clogged gutters. Knowing these causes helps homeowners take preventive measures to reduce water damage and the related financial burden.

1

Severe Weather Events

Severe weather events such as thunderstorms, hurricanes, and flash floods can cause significant water damage to homes. These events can damage roofs and compromise structures, allowing water infiltration and leading to extensive repairs. Flooding from below can cause severe damage, underscoring the need for robust prevention measures.

2

Leaking Pipes and Appliances

Common causes of water damage include leaks or ruptures in washing machines, malfunctioning water heaters, and other appliances. If these malfunctions are not addressed immediately, an entire room can flood in minutes, leading to significant repair costs. Repairing plumbing damaged by water typically costs between $1,000 and $4,000, underscoring the importance of regular maintenance and prompt repairs.

Clogged Gutters and Blocked Drains

Ineffective rainwater management due to blocked gutters can lead to overflow and substantial water damage, emphasizing the importance of regular maintenance. Water damage from blocked drains can have significant financial impacts, including repair costs and potential loss of property value.

How State Regulations Impact Claim Processing

Case Law Reference

A notable legal precedent is Trutanich v. Allstate Ins. Co., 97 Or. App. 514 (1989), where the court ruled that ambiguities in water damage exclusions must be interpreted in favor of the insured. This case emphasizes the importance of reviewing policy language and understanding your rights in a coverage dispute.

Knowing what is typically covered under homeowners’ insurance for water damage is crucial. Generally, homeowners’ insurance covers water damage if it occurs unexpectedly and unintentionally. Common scenarios include accidental damage from burst pipes, malfunctioning appliances, and damage caused by fallen trees.

Flood insurance is essential for mitigating the financial impacts of floods, since most standard homeowner policies do not cover such damage.

Covered Events

Homeowners’ insurance policies provide coverage for various sudden and accidental events that are unexpected. For example, damage from sudden incidents such as a broken washing machine hose is typically covered in homeowners’ insurance claims. Knowing the specific events your policy covers helps ensure adequate protection against potential water damage.

Exclusions

Standard homeowners’ insurance policies typically exclude coverage for flood damage and gradual damage due to poor maintenance. This emphasizes the need to consider additional insurance coverage options for flood-related damage. Homeowners’ insurance also does not cover water damage caused by unresolved maintenance issues, emphasizing the importance of regular property upkeep.

Click to contact our property damage lawyers today

The Role of Flood Insurance

Flood insurance plays a crucial role in covering water damage that standard homeowners’ insurance policies typically exclude. Homeowners should consider purchasing flood insurance for comprehensive flood coverage, especially in flood-prone areas.

The National Flood Insurance Program (NFIP) provides flood insurance to help property owners, renters, and businesses recover from flood events. Without flood insurance, homeowners risk being uninsured for significant flood-related water damage.

1. Costs and Benefits of Flood Insurance

The NFIP offers flood insurance to help property owners recover from flood events. The average premium for flood insurance through NFIP typically ranges from $786 to $888 per year, influenced by factors such as location and flood risk. The benefits of having flood insurance far outweigh the costs, especially considering the substantial financial impact of flood damage.

2. NFIP Claims Statistics

The average payout for an NFIP claim is $52,000, highlighting the significant financial support provided to policyholders. In contrast, the average amount FEMA pays out to disaster-affected homeowners is $4,200, underscoring the importance of having flood insurance for adequate coverage. The average annual cost of NFIP flood insurance is about $700, making it a worthwhile investment for homeowners in flood-prone areas.

Filing a water damage insurance claim involves several crucial steps to ensure a successful outcome. Proper documentation, prompt communication with the insurance company, and taking preventive measures to mitigate further damage are essential. These steps enhance the likelihood of approval and ensure a fair payout.

1

Initial Assessment and Documentation

Documenting the extent of damage is crucial for substantiating your insurance claim. Detailed photos and videos of the damage serve as vital evidence in the claims process. Thorough documentation can significantly enhance the likelihood of a successful claim, ensuring homeowners receive adequate compensation for the damage.

2

Contacting Your Insurance Company

Once the damage has been documented, report the water damage to your insurer as soon as possible to mitigate potential complications. Contacting your insurance provider immediately ensures the claims process begins promptly — crucial for managing repairs and restoration.

Following Up and Mitigating Further Damage

Maintaining regular communication with your insurance provider can help ensure your claim remains active and is processed efficiently. It’s also essential to take steps to mitigate further damage, such as drying out affected areas and making temporary repairs where necessary. A proactive approach can prevent additional damage and support your claim for a fair payout.

Complete a Free Case Evaluation form now

Long-Term Effects of Untreated Water Damage

Neglecting water damage can lead to severe long-term effects that significantly worsen over time. Prolonged water exposure can weaken foundational structures, leading to significant settling and shifting of the home. Untreated water damage can also lead to hazardous conditions, such as mold growth and structural deterioration, potentially rendering the home uninhabitable. Repair costs for untreated damage can quickly escalate, possibly exceeding the home’s value.

1. Mold Growth and Health Risks

One of the most alarming consequences of untreated water damage is mold growth, which poses severe health risks to occupants. Unpleasant smells can indicate that mold is developing, and cabinetry and furniture can begin to weaken and deteriorate within hours of the damage. Mold damage claims are common, emphasizing the importance of promptly addressing water damage to avoid health hazards and additional costs.

2. Structural Deterioration

Prolonged water exposure can severely compromise a building’s integrity. Wooden structures can swell and split, risking their stability, and restorations after weeks of untreated water damage may be extensive and significantly increase costs. Structural issues can include crumbling drywall and loss of building integrity, underscoring the importance of timely repairs.

Summary

According to the Insurance Information Institute, 1 in 50 insured homes files a water damage claim each year, making it one of the most common and costly types of homeowner claims in the U.S.

Understanding the average insurance payout for water damage claims is crucial for homeowners to prepare for potential financial impacts. Factors such as the extent of damage, type of water contamination, and location all significantly influence the payout amounts, and restoration costs can vary widely — emphasizing the importance of adequate insurance coverage.

Homeowners should be proactive in documenting damage, promptly contacting their insurance company, and taking steps to mitigate further damage. Recognizing the long-term effects of untreated water damage, such as mold growth and structural deterioration, underscores the importance of timely repairs. By understanding the nuances of their policies and considering additional coverage options, such as flood insurance, homeowners can better protect their investments and ensure a fair payout.

Frequently Asked Questions

What is the average insurance payout for water damage claims?

The average insurance payout for water damage claims is approximately $11,605. This figure highlights the significant financial impact of water damage on property owners.

What factors influence the amount of insurance payout for water damage?

The payout is influenced by the extent of the damage, the type of water contamination, and the location of the incident. These factors are crucial in determining the compensation you may receive.

What are some common causes of water damage?

Water damage is often caused by severe weather events, leaking pipes and appliances, and clogged gutters. Addressing these issues promptly can help prevent extensive damage to your property.

What is typically covered under homeowners’ insurance for water damage?

Homeowners insurance typically covers unexpected and unintentional water damage, including incidents from burst pipes or malfunctioning appliances. However, it generally excludes damage from flooding or poor maintenance.

Why is flood insurance important?

Flood insurance is crucial because standard homeowners insurance often excludes flood damage. Securing such coverage ensures more comprehensive protection and mitigates the financial risks associated with potential flooding.

Call or text (832) 323-3000 or complete a Free Case Evaluation form