Understanding the statute of limitations for insurance claims is crucial if your claim has been denied or remains unresolved. This period, the statute of limitations, decides how long you have to file a lawsuit against your insurance company. Missing it can permanently bar you from seeking compensation. In this article, we’ll cover the specific time limits, state law variations, the discovery rule, and the key steps to take before the deadline.

Key Takeaways

The statute of limitations sets a strict deadline for filing insurance claims, which varies by state and type of claim; missing this deadline can permanently bar legal action.

Understanding state-specific variations in the statute of limitations is essential for policyholders to protect their rights and file claims on time.

Factors such as the discovery rule and are presence of minors or legally incompetent claimants can affect the statute of limitations, underscoring the need for prompt legal consultation.

For a free legal consultation, call (832) 323-3000

Understanding the Statute of Limitations for Insurance Claims

The statute of limitations defines the period within which you must initiate a lawsuit after an insurance claim is denied or remains unresolved. This timeframe is crucial: if it expires, it generally bars any further legal action against the insurer, regardless of the merits of the claim.

Timely action is vital. Judges do not have the authority to extend the statute of limitations, even if a policyholder faces genuine hardship. Moreover, ongoing negotiations with an insurer do not pause the countdown, making it essential to stay vigilant as deadlines approach.

In essence, understanding and adhering to the statute of limitations isn’t just about knowing the law — it’s about preserving your right to seek justice and compensation. This knowledge can make the difference between a successful claim and a missed opportunity.

State Law Variations on Time Limits

State laws play a significant role in determining the statute of limitations for insurance claims, and they vary widely. Depending on the state and type of claim, the filing window can range from 1 to 10 years — so understanding your state’s specific laws is crucial.

Different types of claims carry different limits. Property damage claims typically range from one to six years, while breach-of-contract claims against insurers often range from three to six years across states.

To illustrate: in New York, homeowners must submit claims within one year of the incident, auto accident victims have three years from the date of the accident, and life insurance claims must be filed within two years. These examples underscore the need to understand the specific limits set by your state’s laws.

Click to contact our property damage lawyers today

The Discovery Rule and Its Impact

The discovery rule is an essential legal principle that can significantly affect the statute of limitations. It allows the clock to begin when the injured party discovers or reasonably should have discovered their injury or loss, rather than at the time of the incident. This ensures people aren’t unfairly barred from seeking justice due to delayed recognition of harm.

The rule is particularly relevant where harm isn’t immediately obvious, for example, hidden water damage that surfaces months later. In such cases, starting the clock from the date of discovery provides a fairer timeframe for claimants.

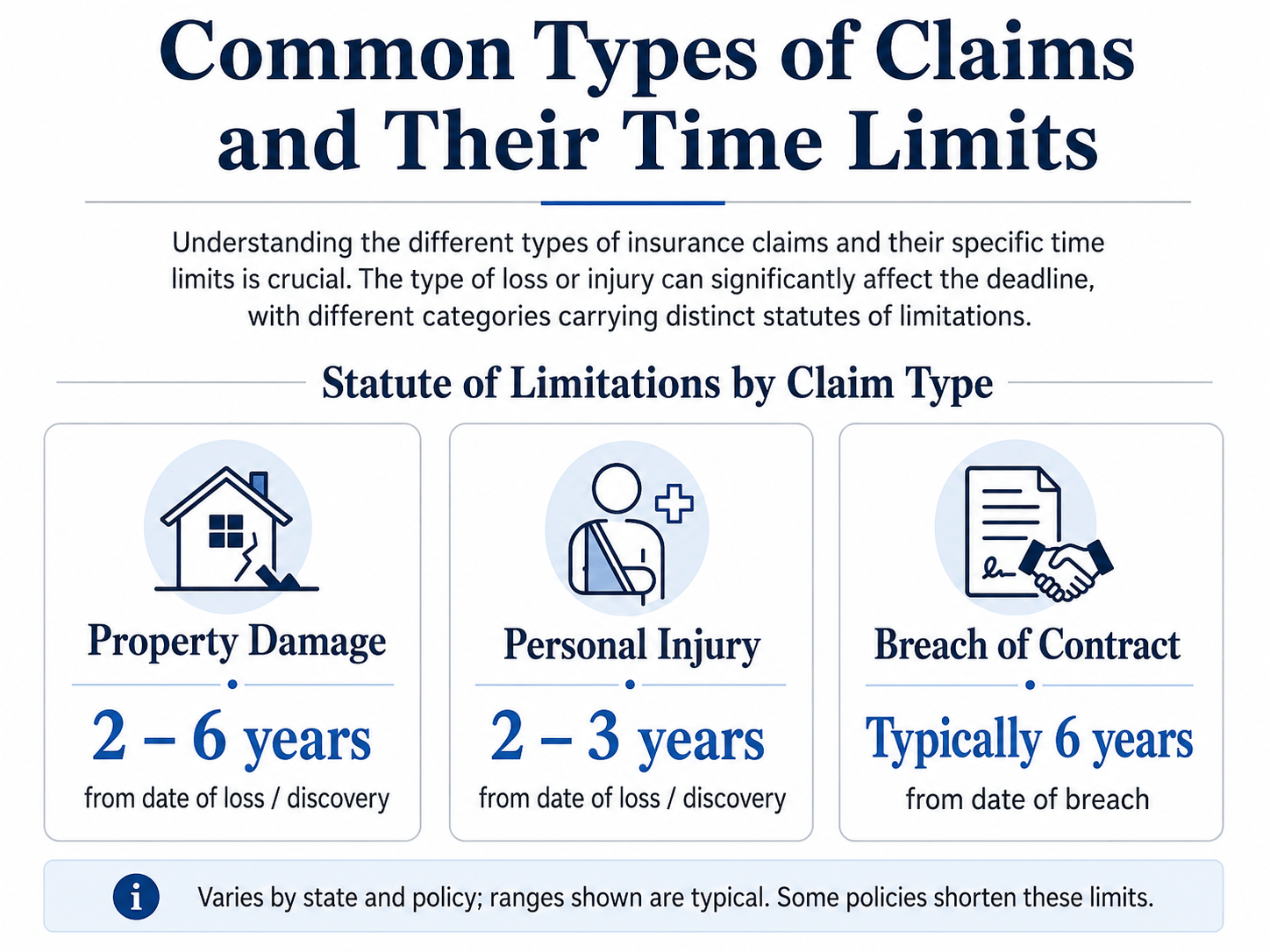

Understanding the different types of insurance claims and their specific time limits is crucial. The type of loss or injury can significantly affect the deadline, with different categories carrying distinct statutes of limitations.

Property Damage Claims

Property damage claims typically have a statute of limitations ranging from two to six years, depending on the jurisdiction. Factors such as when the damage occurred and the timeframe for notifying the insurer can also affect the claim’s validity. Failing to file within the applicable limit can result in the claim being barred — meaning lost compensation for needed repairs — so understanding and adhering to these limits is essential.

Personal Injury Claims

Personal injury claims generally carry a statute of limitations of two to three years, though some states extend this up to six. The clock typically starts on the date of the accident or on the date the injured party becomes aware of the injury. Delays in filing can result in the loss of the right to seek compensation for medical expenses, lost wages, and other damages.

Breach of Contract Claims

Breach-of-contract claims against insurers typically have a 6-year limitation period, starting from the date of the breach. These arise when an insurer fails to uphold the policy, such as by denying a valid claim or failing to provide agreed-upon coverage. Being aware of this six-year window is crucial to preserving your right to pursue legal action.

Complete a Free Case Evaluation form now

What Happens When the Statute of Limitations Expires?

If the statute of limitations expires before a claim is filed, the ability to pursue legal action against the insurer is generally barred completely. Even a valid claim loses the right to compensation, and judges do not have the discretion to waive the deadline.

The expiration can lead to harsh outcomes, particularly when there are disputes over the precise calculation of the limitation period. Even if negotiations are ongoing, the clock keeps running potentially costing you the right to file a lawsuit.

Factors That Influence the Statute of Limitations

Various circumstances can shorten or extend the statute of limitations. If the injured party is a minor or legally incompetent, the clock may be paused. If an insurer engages in fraud or conceals vital information, the limit may be extended. And the deadline may be “tolled” (paused) if the defendant is unreachable or absent. Awareness of these factors helps you navigate the complexities and protect your rights.

Preserving your legal rights requires taking the right steps before the statute of limitations expires.

1

Notify the Insurance Company

Prompt notification is critical — it initiates the claims process and ensures compliance with statutory deadlines. Many policies require claims to be reported promptly to avoid denial, and delays can hinder your ability to receive compensation.

2

Collect Evidence

Gather relevant evidence within the allotted timeframe to substantiate your claim — supporting documentation, such as photographs and receipts, is essential. Organizing and presenting this evidence effectively can improve your chances of a successful claim.

File a Lawsuit

If your claim is denied, filing a lawsuit within the statute of limitations is essential to preserve your legal rights. Consulting an attorney is advisable to ensure all deadlines are met — filing after the statute has expired can lead to dismissal and the loss of any compensation.

Seeking Legal Assistance

Consulting a legal professional promptly is crucial to ensure you meet all deadlines and protect your rights. Delaying can lead to lost evidence and weakened witness testimony, hurting your case. Insurance companies often use tactics to minimize payouts, making early legal representation essential for effective negotiation. An experienced attorney can also help navigate the specific notice requirements that may apply in your state.

Attorney Insights: Strategies for Timely Claims

From the perspective of a first-party insurance attorney, here are essential actions to avoid missing the statute of limitations — and to strengthen your position if litigation becomes necessary:

Send a written demand early. Document your claim with a formal written demand. It shows seriousness, may prompt faster resolution, and helps establish a legal record.

Track all communication. Keep a detailed log of emails, calls, and letters with the insurer. This timeline is vital if a dispute arises over delay tactics or the timing of denials.

Watch for policy-shortened limitations. Some policies include clauses that shorten the standard statute of limitations. Don’t rely on state law alone — read your policy carefully.

Get a legal opinion early. A quick legal review can uncover hidden limitations or tolling triggers, such as fraud or misrepresentation.

Know your tolling opportunities. If fraud, concealment, or the insurer’s absence applies, you may be able to pause the deadline — but you must assert it legally; time doesn’t stop automatically.

Real-World Example

In 2021, a Florida homeowner was denied coverage for hurricane damage. They assumed ongoing negotiations paused the statute — but when they finally tried to sue two years later, the court dismissed the case. The insurer had not formally extended the deadline, and the policy included a one-year contractual limitation. The homeowner lost the right to recover nearly $60,000 in damages due to a technical oversight.

Case Law Spotlight

In Heimeshoff v. Hartford Life & Accident Insurance Co., 571 U.S. 99 (2013), the U.S. Supreme Court ruled that contractual limitation periods in insurance policies are enforceable — even if they expire before a claim could reasonably be filed. This landmark decision underscores the need to read your policy’s fine print and act swiftly, regardless of standard statutes.

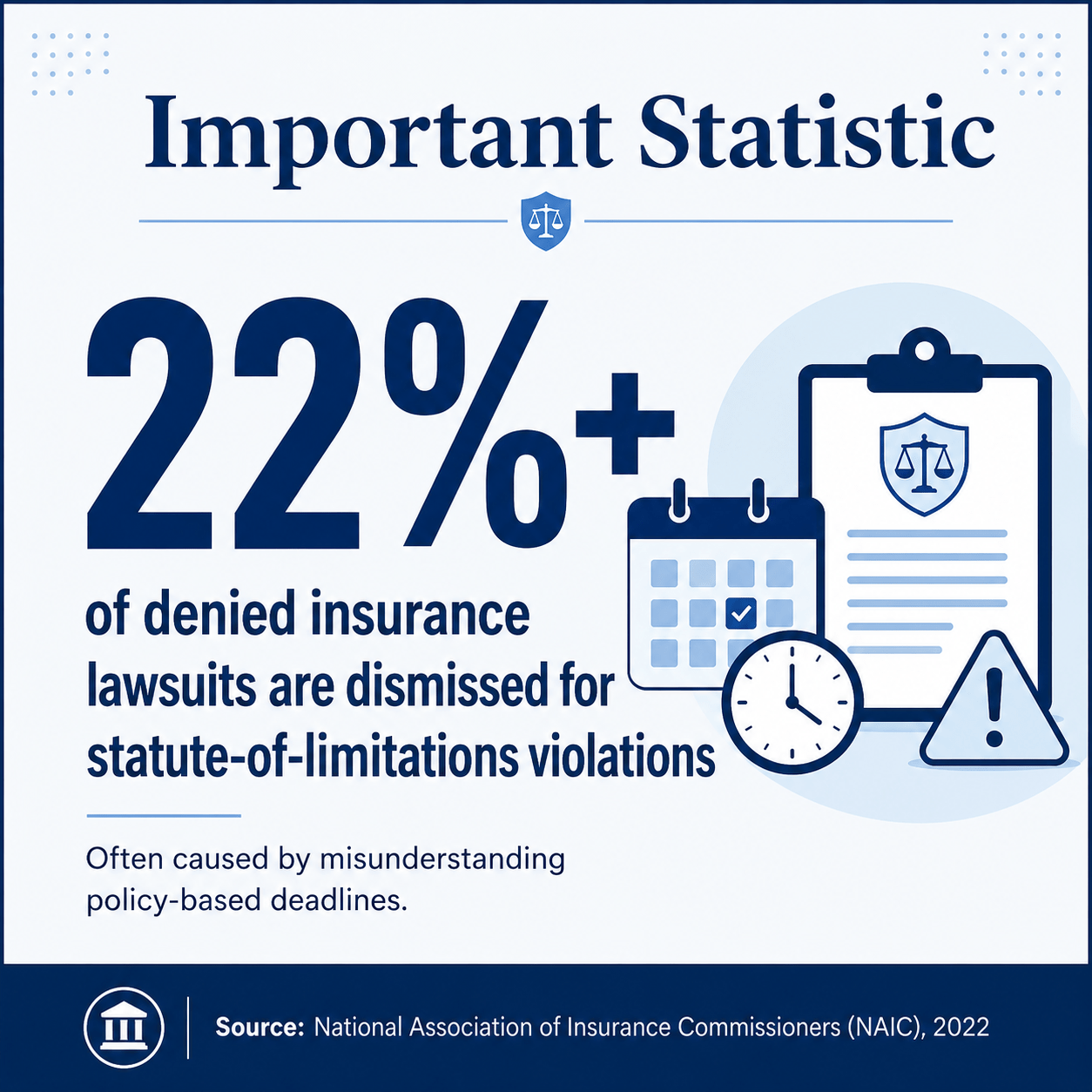

Important Statistic

According to a 2022 National Association of Insurance Commissioners (NAIC) report, more than 22% of denied insurance lawsuits are dismissed due to statute-of-limitations violations — often stemming from misunderstandings of policy-based deadlines.

Summary

Understanding the statute of limitations for insurance claims is essential for protecting your legal rights and ensuring you receive the compensation you deserve. By knowing your state’s variations, the discovery rule, and the specific limits for different claim types, you can take timely action. Remember to notify your insurer promptly, gather necessary evidence, and consult an attorney if needed — these steps will help you navigate the complexities and improve your chances of a successful outcome.

Frequently Asked Questions

What is the statute of limitations for filing an insurance claim?

It varies by state and type of claim, typically ranging from one to six years. It’s essential to know the specific timeframe in your jurisdiction to ensure timely action.

How do state laws affect the statute of limitations for insurance claims?

State laws significantly influence the limit, with time frames ranging from 1 to 10 years depending on the jurisdiction and nature of the claim. Know your state’s specific limits to ensure timely filing.

What is the discovery rule, and how does it impact insurance claims?

The discovery rule starts the statute of limitations when the injured party becomes aware of their injury or loss, allowing a more equitable timeframe for filing, especially for latent harm. It can significantly extend the time available to seek compensation.

What happens if the statute of limitations expires before I file my claim?

You will generally be barred from pursuing legal action, as courts cannot waive the time limit. It’s crucial to be aware of these deadlines to protect your rights.

What steps should I take before the statute of limitations expires?

Notify your insurance company, gather necessary evidence, and file a lawsuit if your claim is denied. Consulting an attorney can provide guidance and ensure all deadlines are met.

Call or text (832) 323-3000 or complete a Free Case Evaluation form