Wondering if home insurance covers roofs? The short answer is: it depends. Homeowners insurance typically covers roof damage caused by specified perils like fire, wind, or hail, but each policy varies, and some damage may be excluded. This article explores what types of roof damage are covered, how to file a claim, and tips for protecting your roof.

Key Takeaways

Homeowners insurance typically covers roof damage from perils such as fire, wind, and hail, but policy exclusions can vary — making it essential to review your specific coverage.

Understanding your policy means recognizing covered and excluded perils — and the importance of regular roof inspections to maintain eligibility for claims.

Filing a roof damage claim requires thorough documentation, prompt communication with your insurer, and a professional inspection to support the claim.

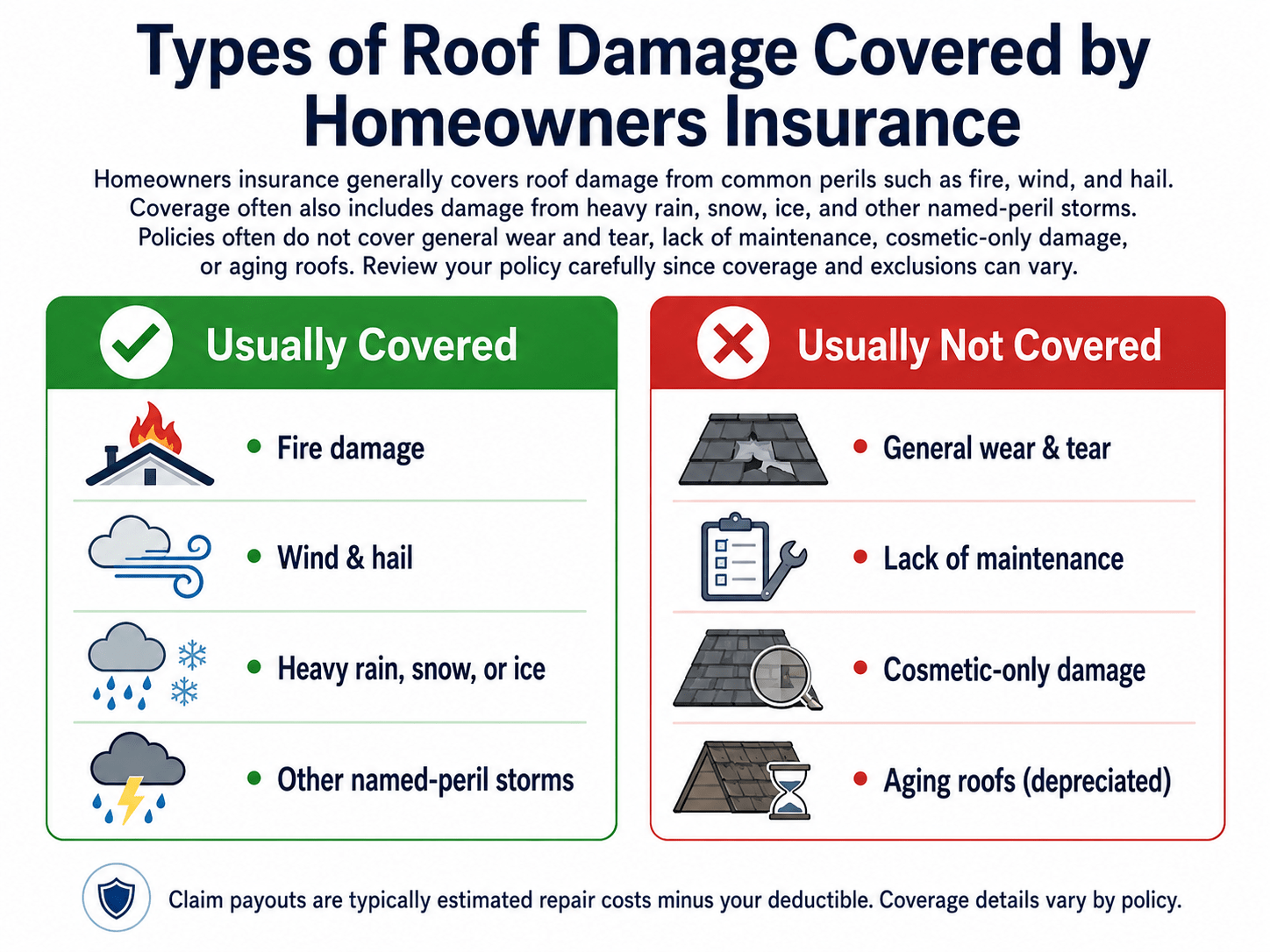

Homeowners insurance generally covers roof damage from common perils such as fire, wind, and hail, which can severely compromise your roof’s integrity. Still, review your policy carefully, since some policies exclude windstorm and hail damage, which can catch you off guard if not anticipated. Comprehensive coverage is the type of car insurance that covers hail damage. It protects against various types of hail damage, such as dents, dings, cracked glass, and interior water damage. As neutral industry sources confirm, rather than liability or collision. Having comprehensive coverage helps cover the repair or replacement of a vehicle due to non-collision accidents like hail damage.

Beyond fire, wind, and hail, coverage often includes damage from weather events like heavy rain, snow, and ice. These conditions can cause significant damage, especially if your roof is older or already compromised.

When your roof suffers damage from a covered peril, your insurer provides a payout for the estimated repair costs minus your deductible, the amount you pay out of pocket before coverage kicks in, which can vary widely between policies. Knowing which perils your policy covers is crucial for adequate protection; reviewing your policy with your agent can offer clarity and peace of mind.

For a free legal consultation, call (832) 323-3000

Understanding Your Homeowners Insurance Policy

Homeowners’ insurance policies can be complex, but understanding them is crucial for proper roof coverage. Begin by checking your policy’s details, focusing on covered roof damage. After any damage, promptly review your policy and contact your insurance agent.

Review your policy to understand both covered and excluded perils. Standard exclusions often include damage from lack of maintenance and general wear and tear, which may lead to claims being denied. Understanding these details helps you avoid unpleasant surprises during the claims process.

Regular roof inspections serve as both a preventative measure and support for insurance claims. An insurance adjuster’s assessment during an inspection helps determine your claim’s viability, and proactive maintenance helps prevent severe damage while keeping your coverage intact.

If your roof is damaged by a covered event, start by filing a claim with your insurer. The process can feel intimidating, but breaking it into steps helps.

1

Assess and Document the Damage

Right after roof damage occurs, limit further harm, for example, cover leaks to prevent more water damage. Inspect for missing shingles, blown-off granules, and debris to gauge the extent of the damage.

Take clear photos and videos to document the extent of the damage, note dates and any mitigation measures, and keep records of emergency repairs (you may be reimbursed by your insurer). Comprehensive evidence supports your claim and speeds up approval.

2

Contact Your Insurance Company

Contact your insurer as soon as you notice roof damage, as delaying can complicate the process. Your agent will guide you in providing details, submitting documentation, and scheduling an inspection. Prompt communication ensures your insurer is aware of the damage and can process your claim efficiently.

Get a Professional Roof Inspection

A professional inspection is crucial — insurers often require an inspection report before approving claims. Prepared by a qualified roofing company, it provides a detailed damage assessment that helps the adjuster understand the extent of the damage and the repairs needed.

Obtain multiple estimates from different roofers before selecting a contractor to ensure a fair assessment of repair costs.

Factors Affecting Roof Coverage

Several factors influence homeowners’ insurance coverage for roof damage. A primary one is the roof’s age: roofs older than 20 years may not be eligible for full coverage, potentially resulting in denial or coverage limited to actual cash value (the roof’s depreciated value), meaning less money for repairs or replacement.

Insurers also assess the cause of damage to determine if it falls under covered perils. Cosmetic damage or wear and tear is often excluded, ensuring only damage from specific, covered events is eligible for a claim.

Other factors include regional weather risks and the balance between cost and coverage. Understanding these helps you make informed decisions and ensure adequate protection for your roof.

Click to contact our property damage lawyers today

Preventative Measures to Protect Your Roof

Preventive measures can reduce the risk of roof damage and help maintain your coverage. Regular inspections and clearing clogged gutters are essential. Hero image — storm-damaged shingle roof, or a roofer inspecting a roof after a storm. Cleaning gutters prevents water from backing up and damaging the roof, a common issue during heavy rains.

Periodic inspections of flashing help catch potential leaks early, and trimming tree branches over your roof prevents storm damage. Ice-and-water barriers can protect roofs from moisture infiltration during winter.

Proper attic and roof ventilation prevents mold and ice dams, and managing downspouts to discharge water away from the roof helps avoid premature shingle aging. These measures protect your roof and help maintain coverage by demonstrating good maintenance.

Complete a Free Case Evaluation form now

Choosing the Right Roofing Contractor

Choosing the right contractor ensures quality repairs and a smooth claims process. After your claim is approved, schedule the work with a trustworthy contractor. Reputable contractors should hold the necessary licenses and carry adequate liability insurance.

Get a written estimate detailing the scope of work and materials, agree on payment terms before work begins (avoid paying in full upfront), and check the contractor’s experience, past projects, and references. The right contractor ensures proper repairs and helps keep your coverage intact.

Customizing Your Roof Coverage

You can customize roof coverage to fit your needs and budget by discussing options with your agent. A Limited Roof endorsement may reduce premiums but provides partial coverage based on the roof’s age and type — cost-effective for managing expenses.

A Better Roof Replacement endorsement allows a roof to be rebuilt using stronger materials after a covered loss (at additional cost), adding peace of mind by making your roof more resilient against future damage.

After replacing your roof, inform your agent so your policy reflects the update — this ensures your new roof is adequately protected and prevents being underinsured.

Attorney Insights: Legal Strategies for Roof Claims

As a first-party insurance attorney, these are the most critical legal and practical tips for homeowners navigating roof damage claims:

Request a certified copy of your policy. This ensures you’re reviewing all coverage terms, including hidden exclusions and endorsements related to roof coverage.

Submit a detailed proof of loss. This legal document supports your claim and can expedite processing, especially for large roof damage claims.

Watch for cosmetic-damage clauses. Some insurers deny coverage by calling damage “cosmetic.” Have a roofer document the structural impact to counter these tactics.

Use meteorological reports. Provide data on weather events, such as hail or wind, on the date of loss to support the legitimacy of your claim.

Get a public adjuster’s estimate. On high-value claims, a licensed public adjuster can help ensure you’re not underpaid — especially when insurers undervalue older roofs.

Real-World Example

In 2023, a homeowner in Missouri had a hail claim denied after the insurer called the roof damage “superficial.” A public adjuster and attorney documented underlying shingle fractures and used NOAA hail data from the storm date. The insurer reversed course and paid out $31,800, covering full replacement and legal costs.

Case Law Reference

In State Farm Fire & Casualty Co. v. Simmons, 963 S.W.2d 42 (Tex. 1998), the Texas Supreme Court held that insurers may be liable for bad faith even when coverage is disputed — if their investigation is unreasonable or biased. This case is central to enforcing fair evaluations of roof claims.

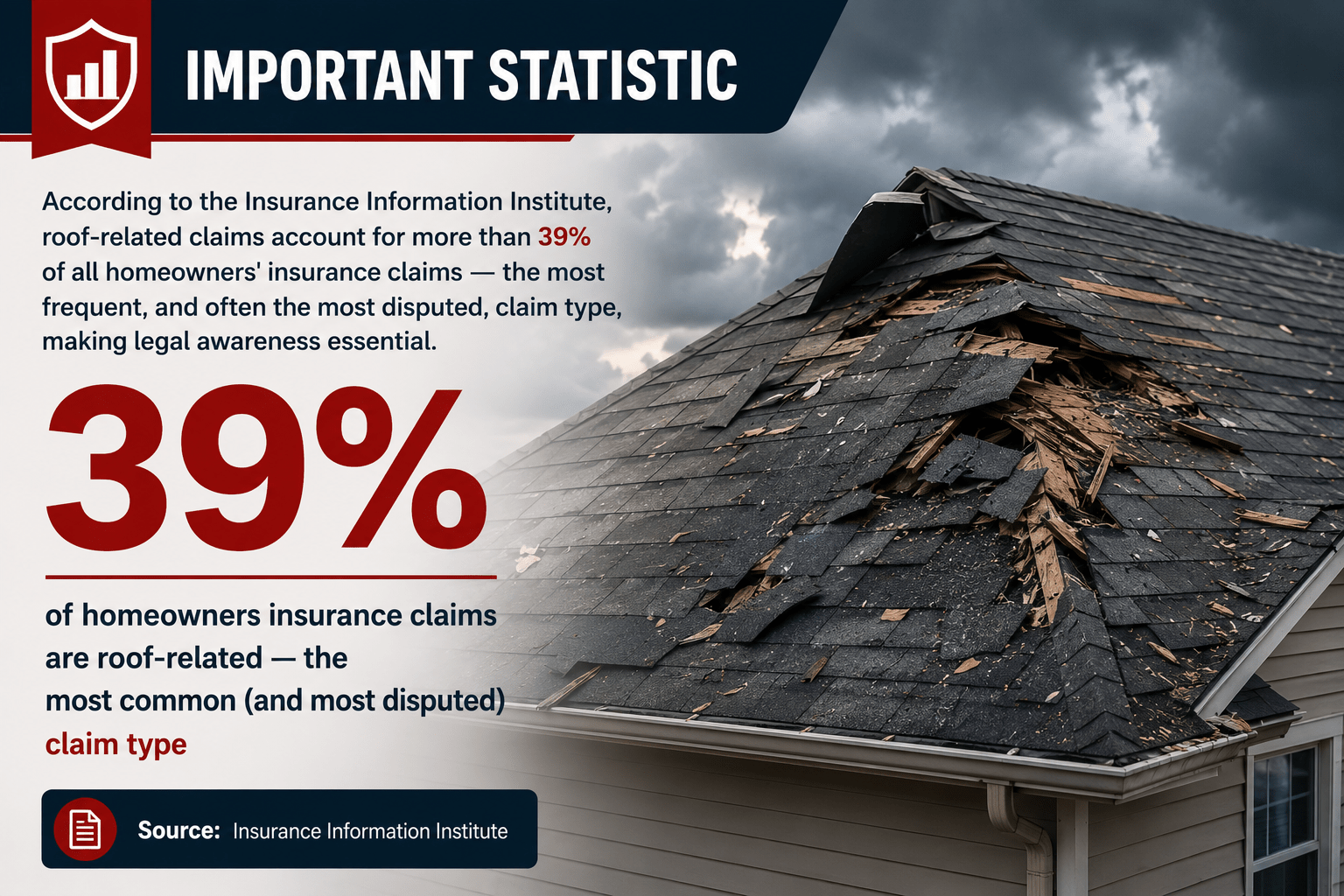

Important Statistic

According to the Insurance Information Institute, roof-related claims account for more than 39% of all homeowners’ insurance claims — the most frequent, and often the most disputed, claim type, making legal awareness essential.

Summary

Understanding homeowners’ insurance and roof coverage is vital for protecting your home. Know what types of damage are covered, how to navigate your policy, and the steps to file a claim. Regular maintenance and choosing the right contractor matter too. Taking proactive measures and customizing your coverage can provide added protection and peace of mind — so stay informed, maintain your roof, and make sure your policy meets your needs.

Frequently Asked Questions

Does homeowners’ insurance cover roof replacements?

Homeowners insurance generally covers roof replacements if the damage results from covered perils such as fire, wind, or hail. Review your specific policy for complete details.

What should I do immediately after my roof is damaged?

Assess and document the damage by taking photos, making temporary repairs to mitigate further issues, and promptly contacting your insurance company.

How can I ensure my roof damage claim is approved?

Maintain thorough documentation, obtain a professional roof inspection, and provide all necessary information to your insurer. This proactive approach significantly increases your chances of a successful claim.

How do I choose a reliable roofing contractor?

Ensure they are licensed and carry liability insurance, obtain written estimates, check references, and refrain from making large upfront payments. This helps you secure quality service and protect your investment.

Call or text (832) 323-3000 or complete a Free Case Evaluation form